A 33 year old real estate agent and investor with over $120M in residential real estate sales. This is my way of sharing actionable ideas that will make you a smarter and wealthier investor.

Top 5 Financial Mistakes to Fix in 2025

Published 10 months ago • 4 min read

What’s up Graham, it’s guys here :-)

I’m now taking consulting calls and offering one-on-one sessions to help with your YouTube channel, Real Estate Deals, Business, or Marketing Strategy (no investment advice).

If you’re interested in booking a call, fill out the form below to see if it’s a good fit. I’ll personally review submissions and select a few people each week for a consultation. These sessions can be held over the phone or via Zoom — your choice.

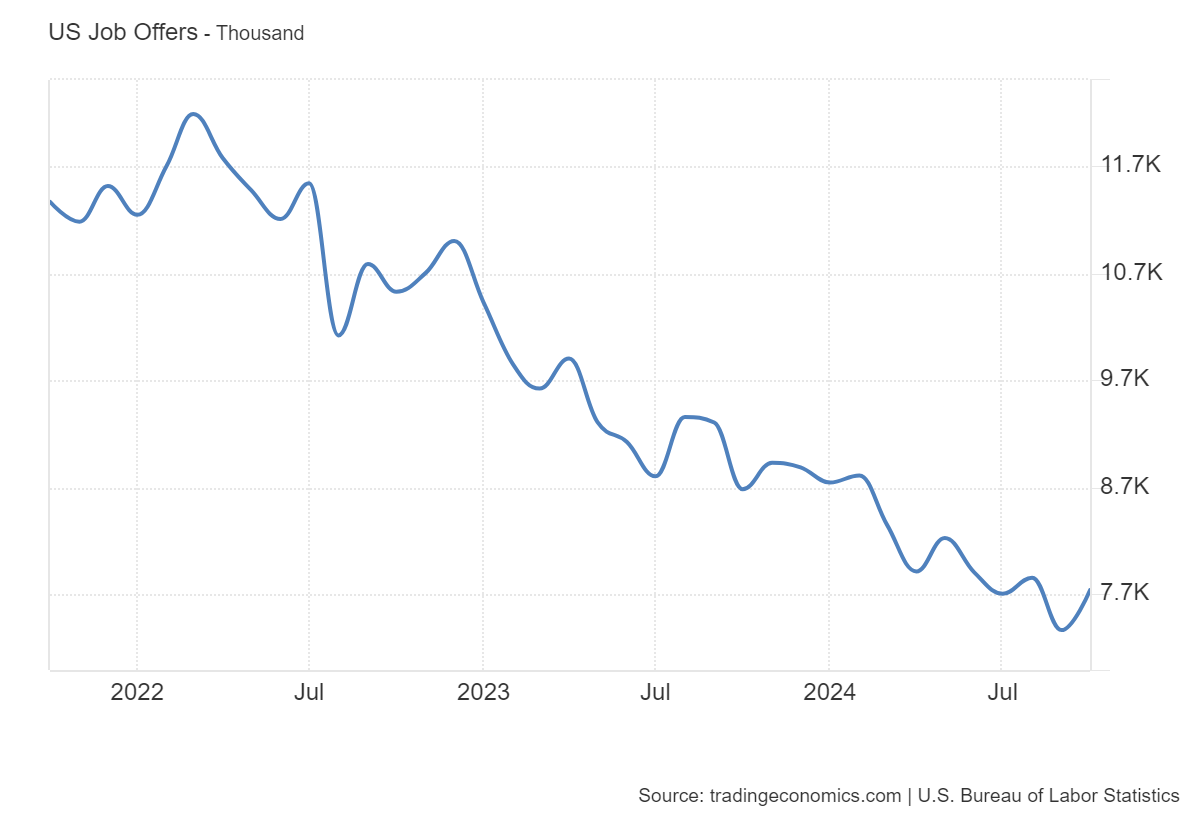

Most people in their 20s make financial mistakes that feel small at the time but can snowball quickly. In 2025, with the Federal Reserve being hawkish, and a poor job market, these mistakes can have an even greater impact if you don’t address them.

Source: Bureau of Labor Statistics

In fact, a recent report revealed that 73% of millennials live paycheck to paycheck, with many believing they’ll never achieve their financial goals. Add to this the growing trends of doom spending and social media-fueled financial pressures, and it’s clear that the need for financial awareness and discipline has never been greater.

The good news? These challenges are fixable. Here are 5 financial mistakes I figured out in my 20s. Fixing these helped me build a solid financial foundation and it can do the same for you in 2025.

Top 5 Financial Mistakes to Fix in 2025

Lifestyle Inflation

Lifestyle inflation is a trap many fall into, especially when they begin earning. It starts innocently: a few nights out, a faster car, or upgrading to designer brands. But before you know it, your spending outpaces your earnings, and you’re dipping into your savings. A study found that 75% of millennials feel social pressure to compete with friends, which leads to unsustainable expenses.

This drains your savings while also limiting your ability to take risks, like pursuing a new career or starting a business. Instead of succumbing to the dinner effect – where one luxury purchase prompts a chain reaction of upgrades – focus on building a financial safety net. Prioritize your needs over your wants and resist the urge to keep up with the Joneses by having a long-term vision of where you want to go.

Not Investing Early

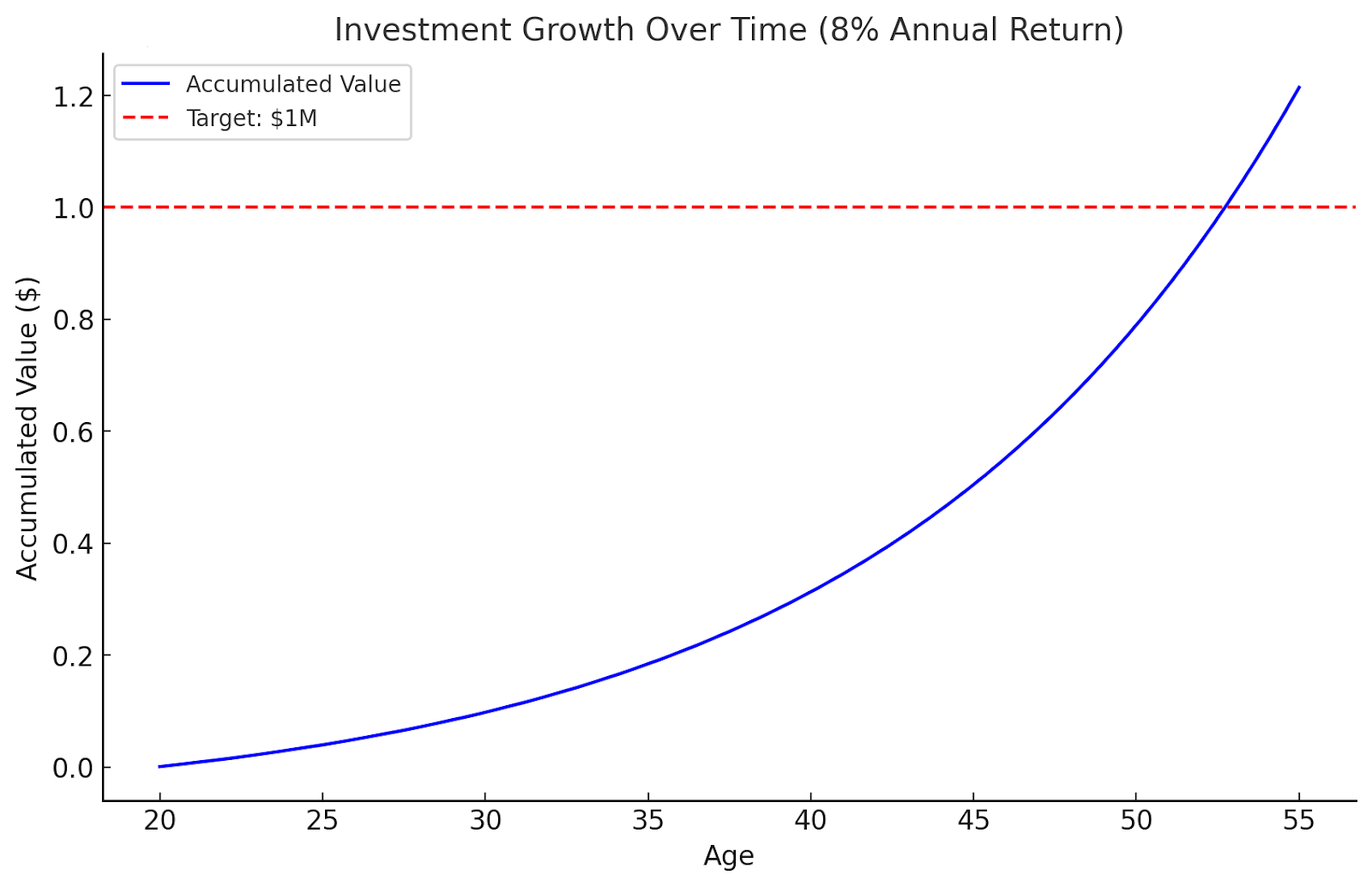

In your 20s and 30s, the biggest investing edge you have is time. Yet many delay investing for retirement, often prioritizing short-term expenses. This leaves you with less money to invest. However, compound interest works best when given decades to grow. The earlier you invest, the more time your money has to grow. Waiting even a few years to start investing can cost you hundreds of thousands of dollars in the long run.

Invest in low-cost index funds, which provide steady returns with minimal effort. Avoid speculative investments like day trading, as data shows that 90% of day traders lose money.

Consider this — If you start investing $500 per month at age 20, you can accumulate $1 million by age 56, assuming a modest 8% annual return. The longer you wait, the more you’ll need to save. Apart from this, consider maximizing your employer’s 401(k) match, contributing to an IRA, and automating monthly contributions. Every dollar saved today will be worth significantly more in the future.

Having a Poor Credit Score

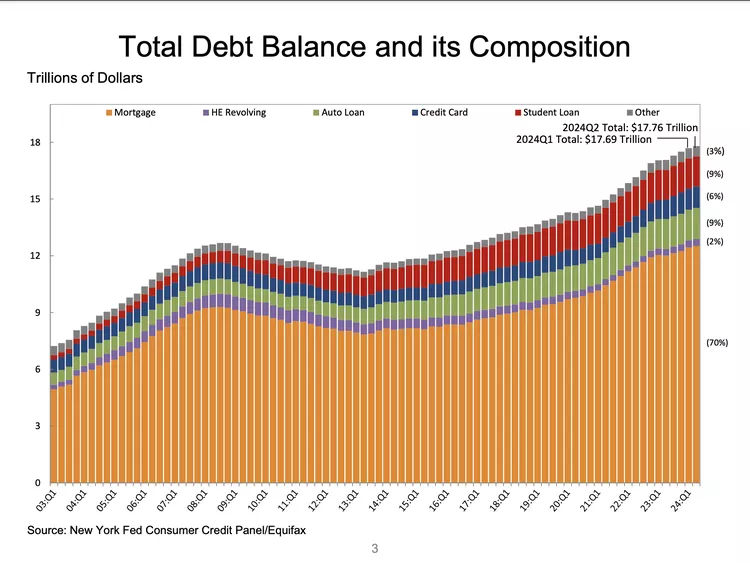

A strong credit score is essential for securing a low interest rate, renting apartments, and even qualifying for specific jobs. Yet many underestimate its importance. Without a credit history, you could face significant hurdles, as I learned firsthand when attempting to purchase my first property. Despite having savings and a steady income, my lack of credit history led to repeated loan rejections.

Student loans, credit card balances, and high-interest debt can severely delay financial progress. The average student loan debt in 2024 was $37,853, and with high interest rates, paying off such debt becomes even more challenging. Building credit doesn’t have to be complicated. Start by opening a no-annual-fee credit card and using it for small, manageable purchases. Always pay your balance in full and on time. Check out my detailed guide to know how I achieved the perfect credit score.

Source: New York Consumer Credit Panel

Not Negotiating

Whether it’s your salary, rent, or major purchases, not negotiating can cost you thousands over time. Many people avoid negotiating out of fear or lack of confidence.

Approach negotiations politely and with preparation. Research market rates, know your value, and don’t be afraid to ask for what you deserve. Often, a simple request can result in significant savings or a raise at your workplace.

Not Budgeting

It’s alarming how many people have little awareness of their financial habits. A survey found that 45% of millennials don’t know how much money they have in their bank accounts. Without a clear picture of your income and expenses, it’s impossible to make informed financial decisions.

Use an expense tracker or budgeting app to categorize your spending. Identify areas where you can cut back and redirect those savings toward your financial goals. To help you get started, here’s a free expense tracker I created to help you crush your 2025 financial goals — 2025 Budget Template.

A few more tips:

Don’t Quit at Your First Mistake: Everyone makes mistakes. Learn from them and keep moving forward.

Don’t Complain: You attract what you focus on. Concentrate on solutions and opportunities rather than dwelling on the negative.

Be Consistent: People overestimate what they can achieve in a year but underestimate what they can accomplish in a decade. Stay the course, and just like investing, let time work in your favor.

Conclusion

Fixing these financial mistakes requires discipline and long-term thinking, but the payoff is worth it. By living below your means, investing wisely, and tracking your expenses, you can set yourself up for lasting financial stability. The path to financial freedom isn’t about perfection; it’s about consistent progress. Start today, and you will thank yourself 10 years down the line.

I’ve had the privilege of working with incredible people through my consulting calls, and the feedback has been amazing. Many have shared how these sessions provided clarity, actionable strategies, and a fresh perspective on their projects — from growing their YouTube channels to figuring out business & real-estate deals.

It’s been incredibly rewarding to see these successes, and I’m excited to continue helping more people achieve their goals. If you’re interested, fill out the Google Form to get started. I look forward to connecting with you!

That's it for this week. I hope you enjoyed this article. Let me know your thoughts by responding to this email - I read every single comment :)

Stay safe, stay invested and I will see you next week – Graham Stephan.

A 33 year old real estate agent and investor with over $120M in residential real estate sales. This is my way of sharing actionable ideas that will make you a smarter and wealthier investor.