What’s up Graham, it’s guys here :-)

A quick but important note before we get started. Since I shifted to ConvertKit, my newsletter is going to the Gmail promotions tab for some of you. If you find this from the promotions tab, please star the message and drag/move it to the primary inbox :)

How I Achieved the (Almost) Perfect Credit Score

Leverage is a fascinating concept. The idea is simple – you borrow resources and use them to expand your potential. Applied wisely, debt lets countries, companies, and even individuals like you and me to grow faster than we could with our limited capital.

Various nations have expanded with the help of leverage -- borrowing money to build infrastructure, finance government programs, and drive economic growth.

However, leverage is a double-edged sword. When not handled properly, debt has also led to the downfall of great empires. Take the European Debt Crisis, for example. Countries like Greece and Italy took on excessive debt when times were good but couldn’t repay it during an economic downturn. This triggered a financial disaster that rippled through Europe.

Debt can be a powerful tool for expansion, but when misused, it becomes a trap. People can miss out on payments, accumulate more debt than they can handle, and find themselves stuck in a debt trap. This is where the importance of managing your debt responsibly comes into play.

In an effort to aid this, credit scores were introduced as a way to measure how well someone handles their own leverage. It helps banks and other lenders assess how likely you are to repay borrowed money over time. A good credit score is essential when applying for loans, mortgages, or even a credit card, as it can impact everything from the interest rates banks offer you to whether you get approved for a loan or a credit card in the first place.

Here are some secrets I used to achieve a near-perfect credit score. These are shortcuts that many people aren’t aware of, and a few of these tips might even pay you for taking advantage of them. In this article, I’ll break down how I achieved a credit score of 847 (out of 850), how your credit score is calculated, and what you need to do to get a good credit score.

How Are Credit Scores Calculated?

Before understanding how to get a good credit score, we need to look at how your credit score is calculated.

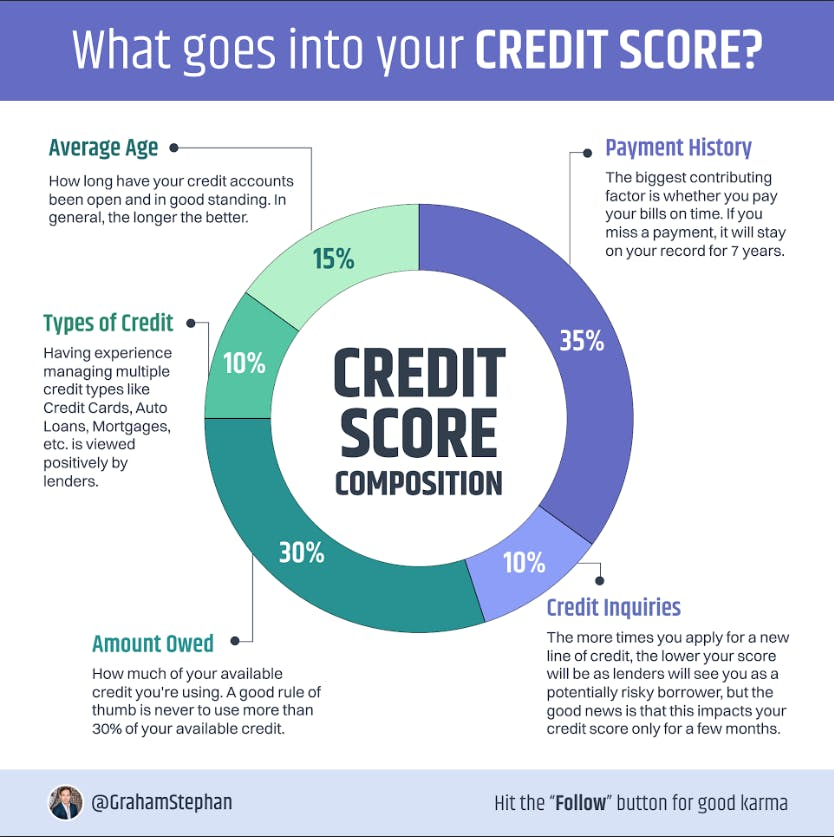

Two major factors affect credit score -- your payment history and your credit utilization rate. Apart from these, your average age of credit, the types of credit you have availed, and the number of credit inquiries a lender has made are also considered. Let’s break it down further:

- Payment History (35%): This simply means paying your debts on time, as agreed, without ever missing a payment. You don’t need to pay off your bills in full—just make the minimum payment, and you’re good. However, it is highly recommended that you make the payment in full to avoid exorbitant interest on the remaining amount.

- Utilization Rate (30%): This measures how much of your available credit you’re using. For example, if you have a $1,000 credit limit and use $100, that’s 10% utilization, which is excellent. But if you use all $1,000, that’s 100% utilization, which is bad.

- Average Age of Credit (15%): The longer you’ve had your accounts open, the better. Lenders see a longer credit history with timely payments as proof that you’re an experienced borrower. This indicates that you’re less likely to default on the payment.

- Types of Credit (10%): Lenders like to see that you can handle different types of loans—whether that’s a mortgage, student loans, or credit cards. It’s not essential to have multiple loans, but it helps.

- Hard Inquiries (10%): Every time you apply for new credit, a hard inquiry is added to your report. Too many inquiries suggest you’re seeking too much credit, which can temporarily lower your score.

Building a High Credit Score

Now that you know how credit scores are calculated, here’s what I did to achieve a high credit score.

- Apply for a No Annual Fee Credit Card

The longer your accounts stay open, the better it is for your credit history. Since you’ll keep these accounts open for years, choose no annual fee cards like the Bank of America Cash Rewards, Discover It Secured, or Wells Fargo Active Cash. These cards cost nothing to keep open and build your credit over time.

- Pay Off Balances in Full

Never carry a balance. Treat your credit card purchases like cash and pay them off as soon as you can before the due date. This helps avoid interest and keeps your utilization low.

- Apply for Another Credit Card After 6-12 Months

Having more credit cards can lower your utilization rate and increase positive trade lines. For example, having two cards and paying both on time doubles your positive trade lines.

- Consider Rewards Cards

After a year of responsible credit usage, apply for rewards cards like the American Express Gold. These cards can pay for themselves and help you earn money through points and perks.

- Add New Lines of Credit Over Time

While not essential, having a mix of credit types (like mortgages, leases, or student loans) can improve your score. You don’t have to go into debt just for the sake of it, but it helps to have a mix.

- Be Patient

If you follow these steps, you should have a high credit score within two years and be approved for almost any loan or mortgage.

For context, here’s what my credit report looks like after YEARS of careful management:

- Payment History: Since 2012, I have had zero late payments, zero accounts in collections, and zero derogatory public records.

- Utilization: I’m using between 0% and 1% of my total available credit. For example, I have a $161,000 credit line and currently owe $38. I tend to pay off my credit cards in full before they’re due because I don’t like seeing balances over $0.

- Average Age of Credit: My oldest account is 12.6 years old, and my average account age is just over 8 years.

- New Credit: I recently opened a credit card over a year ago for a great sign-up bonus, which resulted in a new line of credit and a hard inquiry.

- Credit Mix: I have eight revolving credit card accounts and 13 total accounts, six of which have been paid off in full. I also have $3.8 million in mortgage debt spread across six rental properties, all fixed at or below 4%.

Bonus Tips to Boost Your Score

So far, we've discussed how to build a good credit score from scratch, but now, let's explore how to repair a poor credit score or speed up the process of improving your existing score with more advanced tips.

There are two powerful ways to do that. One is to become an authorized user on someone else’s credit card. By doing this, you leverage their credit history and “piggyback” on their positive credit history. The other way is to pay off overdue loans as soon as possible. If you have a late payment on your report, pay it off as soon as possible to minimize the damage. If you have debt in collections, try negotiating a payment plan with the lender.

At the same time, it’s important to review your credit report for errors regularly. Disputing and removing any inaccuracies can quickly improve your score, as these errors may negatively affect your credit without your knowledge. Tools like Experian Boost can help you track timely payments and add them to your credit report.

Lastly, protect yourself by freezing your credit reports with Equifax, Experian, and TransUnion. This prevents anyone from opening new lines of credit in your name. Freezing your credit is easy and free, and it’s a great way to protect yourself from fraud.

Conclusion

Improving your credit score doesn’t have to be difficult. By following these steps and staying patient, you can achieve a high score and enjoy the financial benefits that come with it.

That's it for this week. I hope you enjoyed this article. Let me know your thoughts by responding to this email - I read every single comment :)

Stay safe, stay invested, and remember: building wealth starts with a solid credit foundation — Graham Stephan.

113 Cherry St #92768, Seattle, WA 98104-2205

Unsubscribe · Preferences