What’s up Graham, it’s guys here :-)

Here's a thought experiment.

| Let's say you bought $15,000 worth of the SP 500 index in October 2008 with no other investments made since then. How much do you think your total portfolio would be worth today? |

|

|

|

|

|

Before you answer this question, take a look at this infographic. It conveys the impact of holding US stocks long term, starting at 5 years:

At first glance, it looks like one might lose a lot of money when buying stocks at a high valuation (like in October 2008). But if you stay invested long enough, the chance of losing money is close to zero. Getting back to the initial poll, if you had invested $15,000 in the S&P 500 in October 2008, it would be worth over $100,000 today.

That’s the beauty of long-term investing — time in the market is more important than timing the market. Even if you start when valuations seem high, the longer you stay invested, the more your returns can be. They can even outgrow your initial investment.

This same rule applies to reaching your first $100,000, too. It might seem daunting initially, but it’s a lot easier than most people think. The key is to start early, stay consistent, and let compounding do the work. If you’ve been wondering how to hit this milestone, even if you're starting from scratch like me, here’s exactly how.

If you like thought experiments like this, you’ll love today’s sponsor. This issue is presented in partnership with my friend Ankur Nagpal's newsletter Silly Money

My friend Ankur is the founder of Teachable (a platform I've used for years).

When Ankur sold his company in 2020, he had no idea what to do with the money he made.

So he ran an interesting experiment:

- He gave half the money to a famous private bank to invest

- He invested the other half himself

5 years later, he wrote an article sharing the results.

Check out the post and subscribe to his new newsletter helping people be smarter about personal finance and taxes.

A Step-by-Step Guide to Saving $100,000

1. Setting the Right Goal

Before you do anything, set a specific target and a timeline. Saying you want to save $100,000 as soon as possible is too vague. Without a plan, that goal could take a few years or even stretch into decades. Instead, set a realistic timeframe that makes sense for your income level and lifestyle. Let’s assume you want to hit $100,000 in three years. That means you need to save around $2,800 a month, $640 per week, or $90 a day.

This might initially sound overwhelming, but adjusting the timeline can make a huge difference. If you stretch it to five years, you’d only need to save about $45 per day while earning an 8% return in the stock market. That’s easily achievable by eating at home instead of going out, just a few times each week. Maybe you have a better idea of where to cut costs. The key is making the math work in a way that feels doable.

2. Start Immediately — No Excuses

One of the biggest mistakes people make is delaying their start. They tell themselves, “I’ll start after this big expense,” or “I’ll begin once I have more money.” But the truth is that most people who delay never actually get around to it, and the best time to start is right now.

Momentum is the strongest when you’re excited about a new goal. If you can take that motivation and turn it into action — no matter how small — you’ll be far more likely to stick with it long-term. Open another savings account today, set up an automatic transfer for SIPs, or start tracking your expenses. Just do something to move in the right direction. Eventually, that momentum will compound and snowball.

3. Track Every Dollar

Once you’ve committed to saving, the next step is understanding where your money goes. Most people have no idea how much they spend each month. That’s why their savings never grow. Using a budgeting app is the easiest way to track your expenses, but if you prefer something more private, I created a free Google Sheet where you can manually enter your spending.

Either way works as long as you stick with it. The goal here is simple: Identify where you’re spending more money and start reducing it. Here are some adjustments you can make today.

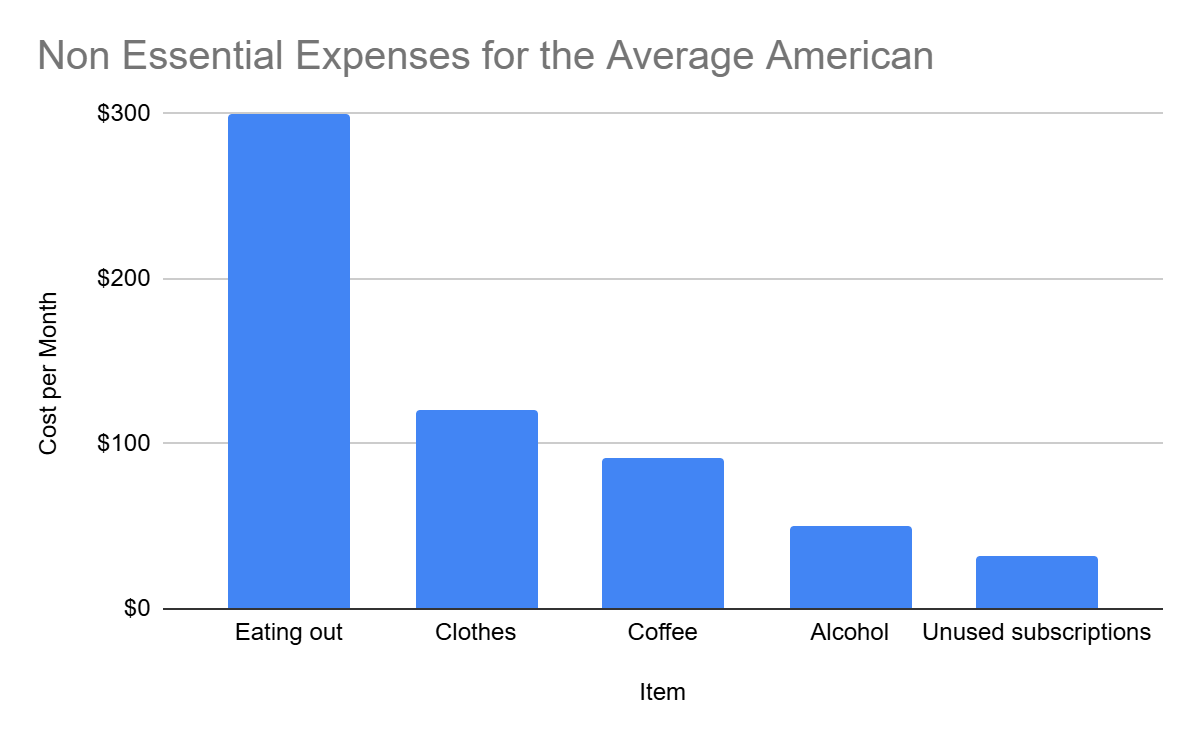

The average American spends $18,000 a year on non-essential purchases. Cutting back on these expenses could free up hundreds of dollars per month to put toward savings. But there’s an even better way to make this process easier, which is Budget optimization.

4. Budget Smarter

Instead of considering cutting back as “sacrificing,” look at it as spending more efficiently. Before making any purchase, ask yourself: How can I get the same thing for less? For example, when was the last time you shopped around for car insurance? With 30 minutes of effort, you could save a few hundred dollars a year while keeping the same coverage. The same goes for internet, phone bills, and even rent.

Another strategy is reevaluating any outstanding debt. If you’re paying a higher interest rate, make it a priority to pay off debt first. Sometimes, banks charge a higher interest rate if your credit score is low. So, the priority should be to increase it. Here’s a detailed guide I wrote on how to improve your credit score.

These minor adjustments quickly add up, and over time, they can easily get you halfway to your savings goal before even thinking about earning more money.

5. Pay Yourself First

One of the most effective ways to ensure you actually save money is by paying yourself first. This means setting up an automatic transfer to your savings account before spending anything for the month. Most people take the opposite approach: they spend first and save whatever is left over. The problem here is that there’s rarely anything left at the end of the month. If you treat savings as non-negotiable, like rent, you’ll hit the goal much faster. This is especially important because most people have a spending problem, not an income problem.

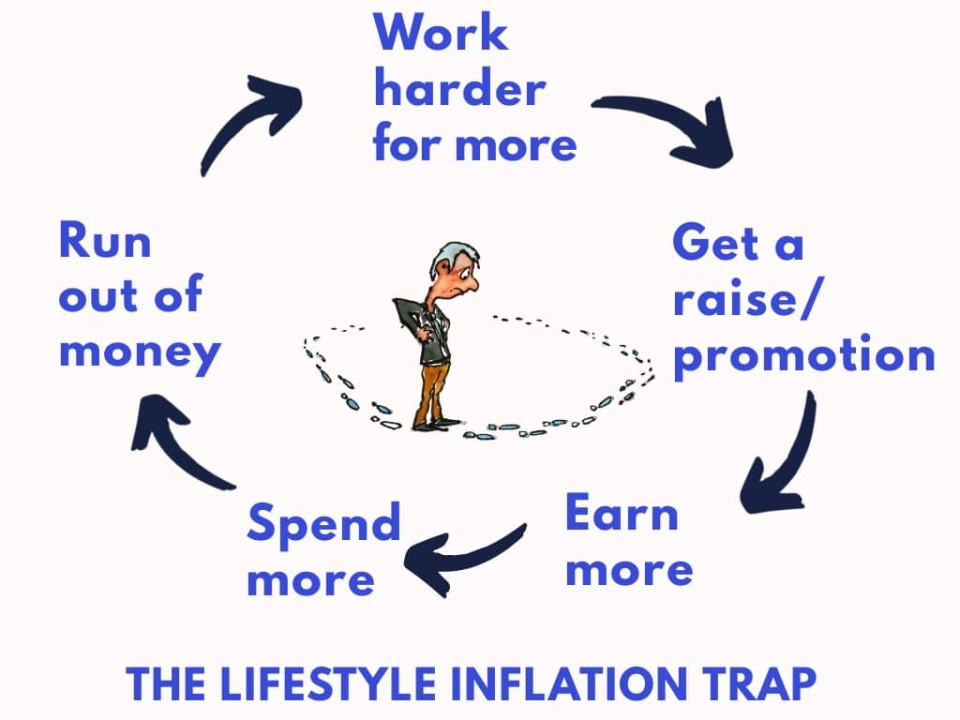

For example, 35% of people making $50,000 annually live paycheck to paycheck. But guess what? The same 35% of people making $200,000 annually also live paycheck to paycheck. The issue isn’t income — it’s lifestyle inflation. When people earn more, they spend more, which is why so many people struggle to save. By automating your savings and keeping track of expenses, you’ll ensure that every dollar you earn works for you and not the other way around.

6. Increase Your Income (Without Overworking)

Cutting your expenses is a start, but at some point, earning more is the best way to increase savings. The easiest way to do this is by asking for a raise, negotiating better pay, or taking on extra hours at your current job.

If that’s not an option, switching jobs often leads to substantial pay increases. Research shows that job hoppers earn an average of 35% more over three years, so if you’re underpaid, it might be time to explore new opportunities.

The Final Step

Yes, saving $100,000 takes effort, but it’s completely possible by focusing on small, consistent actions. Track your spending, automate savings, and increase your income. Once you’re consistently saving, investing takes it to the next level. Historically, the S&P 500 has returned 8% per year, which means the sooner you start, the easier it becomes to grow your money. Even after reaching your goal, $100,000 invested at an 8% return over 30 years turns into $1 million. That’s the power of compounding.

That's it for this week. I hope you enjoyed this article. Let me know your thoughts by responding to this email - I read every single comment :)

Stay safe, stay invested and I will see you next week – Graham Stephan.

113 Cherry St #92768, Seattle, WA 98104-2205

Unsubscribe · Preferences