In 2016, Akagi Nyugyo, a Japanese frozen dessert maker, released an unusual commercial. It showed the company employees and executives bowing down in apology, expressing regret.

The reason?

For the first time in over 25 years, the company increased the price of Garigari-kun, their best-selling popsicles, from ¥ 60 to ¥ 70 — an increase of roughly 7 Cents. The company wanted to apologize for this price hike. The company did it again when they raised the price from ¥ 70 to ¥ 80. And this is not a one-off instance. Another famous confectionary company, Chirin, said it had been feeling the pinch of worldwide price increases, which forced it to raise its prices.

In a country where deflation, economic stagnation, and low interest rates have been the norm for decades, price increases are a big deal. Japan’s economy has always been a curious case. For years, it has had near-zero or even negative interest rates, all to spur growth and combat deflation.

However, the Bank of Japan recently made a surprising move by raising interest rates, breaking with years of economic tradition. This simultaneously led to the “perfect storm” of events, causing some of the largest single-day losses in the stock market since COVID-19.

In this article, let’s break down exactly what’s happening, why the market is in freefall, what you need to look out for, and what history tells us is most likely to happen next since this is rather unprecedented.

The Carry Trade Conundrum

Even though this sounds like a complicated term, it’s easy to understand once we break it down. Global economies are highly interconnected. When one country is economically stronger than another, money tends to flow out and into something else — more often than not, the US Dollar.

Even though the American Dollar has lost a significant portion of its purchasing power over the last 50 years, it’s still the “Reserve Currency” of the world, leading to a consistent demand for US-backed treasuries.

Every country has its own currency, interest rate, and inflation, which are constantly measured against what you can buy in US Dollars. This means there can be arbitrage opportunities where you can borrow one currency at a lower interest rate, earn a higher interest rate in another currency, and then profit from the difference — exactly what had been happening with Japan.

Japan's Economic Struggles and the Impact on the US Dollar

For more than 30 years, the value of the Japanese Yen has been declining against the US Dollar. Japan’s economy has been struggling with deflation, an ageing population, and weak demand. This has led to significantly low interest rates to incentivize spending, borrowing, and trade, which is why Japan’s inflation rate is practically zero.

However, because the United States battled record-high inflation throughout 2022 and 2023, it was forced to raise interest rates at the fastest pace ever in history. Suddenly, US treasuries were paying much more interest than other countries’ investments, making them an attractive, “risk-free” opportunity.

Traders could now borrow the Japanese Yen at a low interest rate, buy US treasuries with this loan, and profit from the difference.

On top of that, the Yen had been losing its value against the US Dollar, meaning investors could pay off their debt with fewer US Dollars than they initially borrowed.

That was the case until recently.

Japan Raises Interest Rates

Since the Japanese Yen consistently lost value against the US Dollar, AND you could borrow at a significantly lower interest rate, it also meant that you could pay off your debt with fewer US Dollars than you initially borrowed.

However, when Japan raised interest rates, it resulted in significant losses for those who had borrowed in Yen to invest in US Dollars.

Imagine you borrowed ¥ 1.6 million to buy $10,000. When you have to pay back the loan, the stronger Yen means that $10,000 only gets you, say, ¥ 1.4 million, leaving you short by ¥ 200k.

This is precisely what happened last week.

Investors had to compensate for this short-change, which led to a massive selloff in the stock market. Trillions of Dollars had to be sold to pay off loans that now cost more to repay than what was initially estimated.

Why Did Japan Raise Rates?

Many people wonder why Japan would raise interest rates if it would cause such turmoil. The answer is inflation — not just inflation, but record inflation.

As the Yen decreased in value, Japan’s exports became more expensive, putting pressure on its economy. It had to act quickly to prevent its currency from falling further. The easiest way to probably do that is to raise interest rates.

This combination of events led to an abrupt selloff, causing the NIKKEI to fall 13%, its biggest single-day loss since Black Monday of 1987. In comparison, the US markets only dropped around 3%.

However, this isn’t the only factor at play — we also have recession fears.

Recession Fears and the Labor Market

Last week, it was announced that US companies were no longer hiring at the rate initially expected. The unemployment rate increased to 4.3% — the highest since October 2021 — signalling that a recession might be on the horizon.

We also have the SAHM Indicator, which measures how quickly unemployment rises. Historically, when unemployment increases by half a percentage point from the previous year, a recession is either imminent or already happening.

This signal was triggered after the disappointing jobs report, suggesting we may be heading into a recession.

This unemployment rate and fear of a recession have a massive impact on industries, including oil, which recently fell to $73 a barrel due to concerns about weakening demand and rising unemployment.

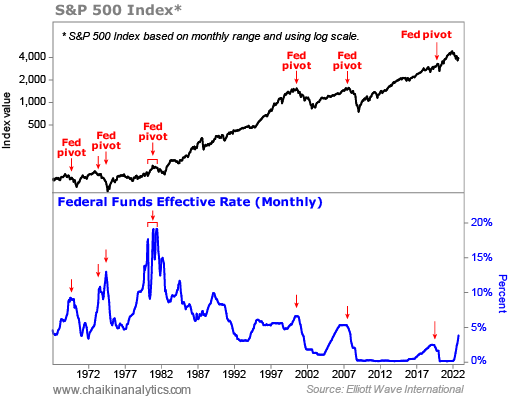

Potential Rate Cuts and Market Implications

In light of all this, some economists are calling for an emergency rate cut from the US Federal Reserve to soften the blow. Others believe the Fed is too late and should have acted sooner. The market is currently pricing in a 50 basis point rate cut as early as September, as discussed in last week's newsletter.

Historically, the Federal Reserve hasn’t dropped rates unless absolutely necessary. They drop rates in anticipation of events that could be disastrous for the economy, almost as a way to help soften the blow before things get too bad.

While rate cuts can often signal trouble, there are plenty of instances where an uncertain market eventually begins to recover, some of which have the potential to produce substantial returns.

How to Prepare for Market Uncertainty

How should you prepare for this uncertainty? Here’s what I’d do myself:

- Keep a 3-6 Month Emergency Fund

Always have enough cash to cover your expenses for 3-6 months. This ensures you won’t need to sell investments when the market is down.

- Diversify Your Investments

Spread your money across different sectors and assets. Don’t put all your eggs in one basket, whether stocks, crypto, gold or anything else.

- Keep Buying In

It’s tempting to stop investing when the market drops, but studies show that the best approach is to keep buying. Bull markets always follow downturns, and sticking to your plan will pay off in the long run.

- Don’t Panic Sell

Panic selling is one of the worst mistakes investors can make. If you sell at the bottom and try to time the market, you'll likely miss out on recovery. Remember, time in the market > timing the market.

- Keep a Steady Income

The most significant risk during market corrections is losing your job. Make sure you have a steady income to continue investing or cover your expenses, or at least cover your expenses without selling your assets.

- Consider Holding Extra Cash

If you’re risk-averse, keeping more cash on hand can provide peace of mind. This is less about optimizing returns and more about feeling secure.

- Think Long-Term

If you need the money in the next 3-5 years, don’t invest it in stocks. Stocks are long-term investments, and short-term fluctuations can leave you with losses if you need to sell early.

At the end of the day, all of this is the result of several negative factors influencing the market simultaneously.

The market may drop further or recover sooner than we expect. What’s important is to stay the course, not panic, and remain prepared for whatever happens next.

That's it for today. I hope you enjoyed this article. Let me know your thoughts by responding to this email - I read every single comment :)

Stay safe, stay invested, and I will see you next week – Graham Stephan.

That's it for this week. I hope you enjoyed this article. Let me know your thoughts by responding to this email – I read every single reply :)

Stay safe, stay invested and I will see you next week – Graham Stephan.

113 Cherry St #92768, Seattle, WA 98104-2205

Unsubscribe · Preferences