A 33 year old real estate agent and investor with over $120M in residential real estate sales. This is my way of sharing actionable ideas that will make you a smarter and wealthier investor.

The Federal Reserve Announces the Rate Cut

Published about 1 year ago • 5 min read

Hey there! A quick announcement:

Now that my schedule is slightly more flexible, if you’re interested in booking a consulting call and speaking with me directly, fill out the form below to see if it’s a good fit.

I’ll make some time each week to speak with a few of you, one-on-one, about your YouTube channel, Real Estate Deal, Business, or Marketing Strategy (no investment advice). If you’re interested, reach out and I’ll pick a few people to consult with. It can be over a phone call or Zoom (your choice). Thanks for reading!

We’re about to see a paradigm shift. Even though the Federal Reserve announced another rate pause last week, the market believes we could see the first rate cut as early as this September.

The market is bracing itself to be completely overturned, for political reasons. With new proposals coming in every week, including nationwide rent control, we should break down exactly what this means, what’s most likely to happen, and how this is going to impact you.

Rising Prices

In terms of an upcoming rate cut, let’s first address what’s triggering it – inflation.

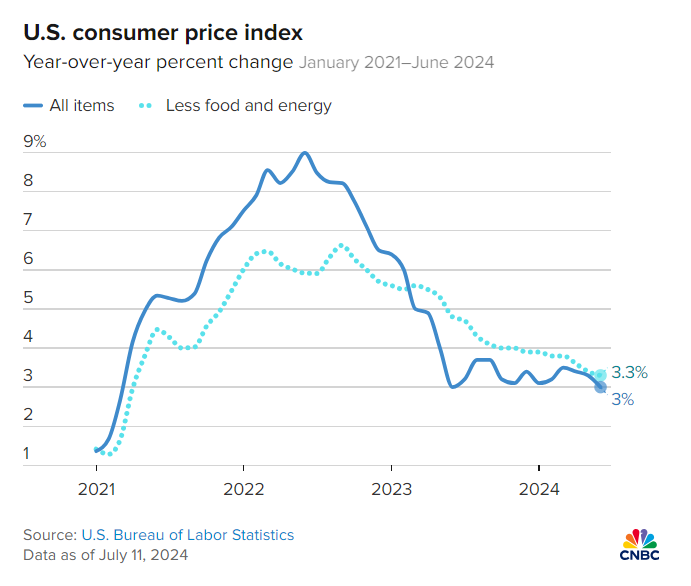

Even though consumer prices have risen by an average of ~ 21% since 2020, there is some good news —prices in June 2024 fell for the first time since the start of the pandemic.

Even though it was only a drop of 0.1%, the trend is clear: Inflation is quickly falling. All items increased at just 3% year-over-year, and if you remove food and energy, we’re practically back to the same inflation levels we saw in early 2021.

Source: CNBC, U.S Bureau of Labor Statistics

This means inflation is finally subsiding, and higher interest rates are ending. If this continues for a few more months, it could also mean a substantial rate cut by the Federal Reserve.

Or could it?

To break this down, let’s focus on a topic that has never been more relevant than it is right now:

The Stock Market and Political Parties

On one side, we currently have Democrats, who have led the S&P 500 with a nearly 20% gain from its low in October 2023. On the other side, we have Republicans, with Trump proposing a massive corporate tax cut that could spark another economic boom.

This leads us to the question: Historically, who has been better for stock market returns — Democrats or Republicans?

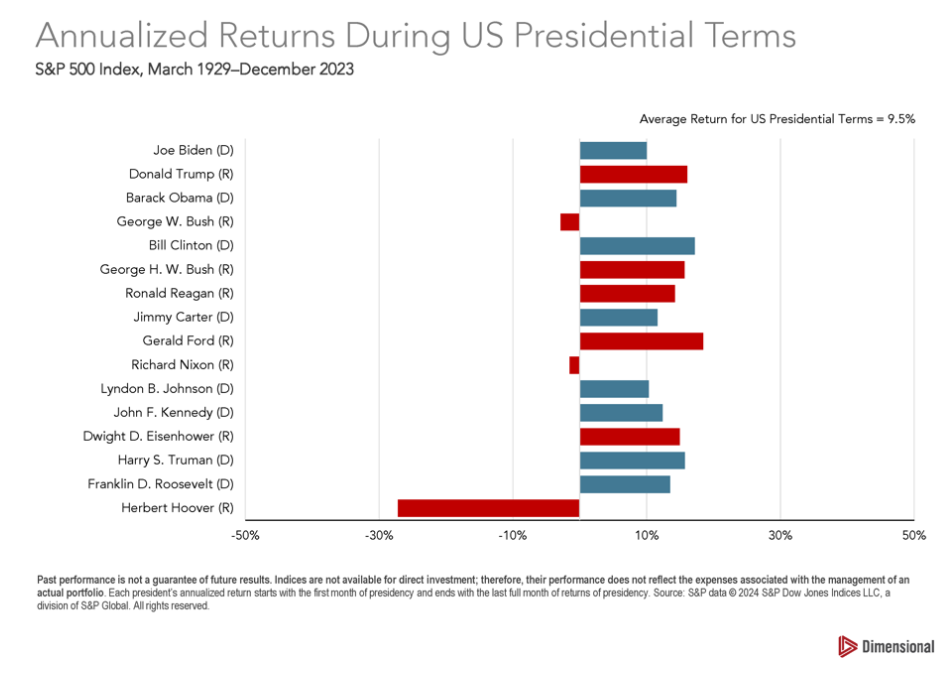

Note: Past results don’t always indicate what happens in the future, and the president doesn’t have direct control over the stock market. This is not an endorsement for any political party; it is just research presented as is.

Source: Dimensional

Over the last 100 years, only three presidents have ever experienced negative returns of the SP500 on an annualized basis over the course of their term: George Bush, Richard Nixon, and Herbert Hoover who happened to be in office through the Great Depression.

Apart from them, every other president has seen positive returns while in office. Another trend is that election years are the most profitable.

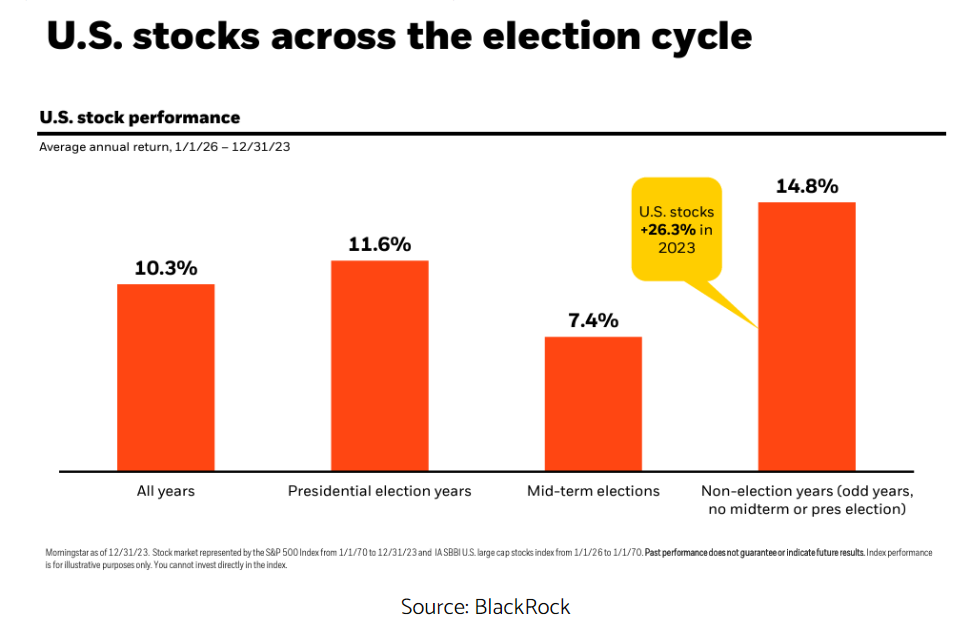

During the same time period, the stock market has averaged a 10.3% annualized return. But if you isolate presidential election years alone, that jumps to a staggering 11.6% return. Investors are the most cautious around mid-term elections, with the market increasing just 7.4% compared to non-election years when it averages 14.8%.

What’s the explanation for this?

Well, if there’s anything an investor hates, it’s uncertainty. When the market can’t price in “the unknown,” it tends to divert to the worst-case scenario, and as a result, average returns fall—especially when Congress has a much larger impact on the overall economy than the sitting president.

However, which political party is “better” for the stock market depends on whose data you look at.

YCharts found that the average Democratic President saw the market achieve an 8.72% return when both the House and Senate were majority Democrats, 15.72% with a split Congress, and 14.55% with a Republican Congress. On the other hand, Republican Presidents achieved a return of 11.7% with a Republican Congress, 12.2% with a divided Congress, and just 1.04% with a Democratic Congress.

Historically, a mixed Congress seems best for the markets because any radical proposals won’t pass, leading to more stability. This brings us to yet another radical proposal currently at hand.

Impact on Housing Prices

Home sales have hit yet another record high, rising 4.1% nationally from a year ago. However, they’re growing at the slowest pace since early 2023. The NAR’s chief economist stated that we’re seeing a slow shift from a seller’s to a buyer’s market. Supply and demand dynamics are nearing a balanced market condition, implying that the days of massive price gains are likely behind us. It’s now cheaper to rent than in all 50 of the largest US metros.

To help reduce the rising cost of rent, Congress is proposing a bill on nationwide rent control. Under this new proposal, the president calls on Congress to cap rent increases on existing units by 5% or risk losing current federal tax breaks.

Landlords who use federally backed mortgages will have to comply with additional regulations, including a 30-day notice before rent increases, a 30-day notice on lease expiration, and a 5-day grace period before imposing late fees on rental payments.

The Effectiveness of Rent Control

Rent control, in theory, would prevent landlords from raising prices on already financially-burdened tenants. However, rent control has been found to make the housing situation worse.

A 1992 poll of the American Economic Association found that 93% of its members agreed that a rent ceiling reduces the quality and quantity of housing available in the market. This is one of the very few things economists universally agree on.

According to a more recent Stanford study, rent control has an adverse effect on making housing more affordable. Rent-controlled tenants were 20% more likely to stay in their unit, renters were more likely to move elsewhere without rent control, and turnover was highest in the priciest neighborhoods as landlords tried to remove tenants to achieve market rents. This results in a lower supply of new units in the market.

While some renters may get a bargain, most people never get access to low rent-controlled prices. Rent control also decreases the income and local property taxes that landlords pay, which ultimately flow back into the community.

I agree with policies that require sufficient notice to raise rents or a grace period before imposing late fees. Those are beneficial and SHOULD be the industry norm. But the ONLY solution for lowering rents or providing affordable housing is to build more through developer tax incentives or less restrictive zoning. That’s it. This is just a classic case of supply and demand.

Realistically, this bill most likely won’t pass through Congress. It’s more akin to political posturing than a genuinely viable solution, but that’s government for you. Speaking of the government, let’s look at what Jerome Powell said:

Jerome Powell’s Recent Comments

Jerome Powell’s recent comments were more favorable than those of past meetings. Although the Federal Reserve didn’t outright say they’re lowering interest rates at the next meeting, they gave clues that they can reduce rates if inflation continues on a downward path.

The labor market is slowly beginning to soften, with fewer job openings than before. Inflation is on a downtrend, meaning the Federal Reserve has done an excellent job of controlling it. They’re not going to promise a rate cut until their next meeting, which is September 18th, but assuming all data points align in the right direction, it’s looking rather optimistic.

Jerome Powell reassures everyone that they will be data-dependent, take it slow, and make their decisions meeting by meeting. It seems that all indicators point to a 25 basis point rate reduction in September. However, even if we see a rate cut, expect them to take it very slowly and cut only when they’re 100% confident.

This likely means higher rates for longer, and it may take another year or two for the federal funds rate to normalize to around 3.1%, which – they project – will occur around 2026.

That's it for this week. I hope you enjoyed this article. Let me know your thoughts by responding to this email - I read every single comment :)

Stay safe, stay invested and I will see you next week – Graham Stephan.

A 33 year old real estate agent and investor with over $120M in residential real estate sales. This is my way of sharing actionable ideas that will make you a smarter and wealthier investor.