A 33 year old real estate agent and investor with over $120M in residential real estate sales. This is my way of sharing actionable ideas that will make you a smarter and wealthier investor.

Why Some People Succeed Financially

Published 9 months ago • 6 min read

What’s up Graham, it’s guys here :-)

In partnership with 1440:

News. Without Motives. That’s 1440.

Over 4 million readers rely on our 5-minute newsletter for a clear, fact-based view of the world. We sift through 100+ sources to bring you unbiased news on politics, global events, business, and culture. Free of charge and free of bias.

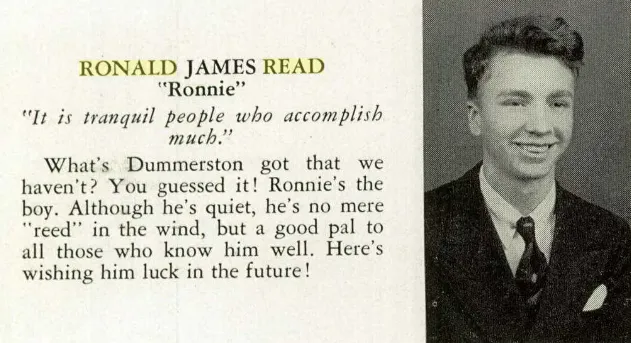

I read about Read on Reddit a while ago, and his story stuck with me ever since. He wasn’t a Wall Street banker, an entrepreneur, or a Fortune 500 CEO. He was a janitor and a gas station attendant from Vermont, who lived a quiet, unassuming life.

Upon graduation, he was enlisted during World War II. When he returned home, he spent decades working as a janitor & a gas station attendant. He drove an old Toyota and rarely spent money on luxury items. To those around him, he seemed like an ordinary blue-collar worker getting by on a modest income.

But when he passed away in 2014, the town of Brattleboro was stunned. Read quietly amassed a fortune of over $8 million. His secret wasn’t winning a lottery or a hidden inheritance — it was a handful of simple, disciplined habits that helped him become a multi-millionaire.

He lived frugally, and regularly invested in blue-chip stocks that he knew well. Read avoided companies that he did not understand, and preferred dividend paying companies. Over time, these small but consistent actions added up, allowing him to build a multi-million dollar fortune without taking on unnecessary financial risks.

Ronald Read in the 1940 Brattleboro High School yearbook | Source: Wikipedia

The good news is that anyone can follow this model — you don’t need a high-paying job, an advanced degree or win the lottery. You can build your financial freedom one step at a time, regardless of your current income or experience. This is why, in this article, I’ll share nine essential financial habits that helped me avoid common money pitfalls and steadily grow my own wealth over the years.

Financial mistakes you must avoid at all costs

1. The Silent Wealth Killer

One of the biggest mistakes people make is increasing their spending as their income rises. It starts small — upgrading your car, eating out more often, buying nicer clothes. But before you know it, those luxuries become necessities, and suddenly, you need more money just to maintain your lifestyle. Personally, I was aware of this throughout my 20s and kept my expenses low. Now, because of these sacrifices, I can afford the lifestyle I want without any financial stress. The key is simple — keep your expenses low and save the difference.

2. Not Tracking Expenses

If there’s one thing that separates financially successful people from those who struggle, it’s this: one group tracks its expenses, the other doesn’t. The average American spends $18,000 a year on non-essential items and $300 a month on impulse purchases. If you’re not already financially secure, you shouldn’t be doing this.

Start by tracking your income and expenses for 60 days using a free tool like this Google Sheet. Think of this like your financial check engine light — if something is wrong, this will tell you exactly where to look. Most people completely ignore it, which is why they stay stuck. If you do this for two-three months, I guarantee you’ll be shocked at where your money goes and how much you can save.

3. Borrowing the Maximum You Can Afford

Lenders are in the business of loaning you as much money as possible. They stretch out the loan tenure to make large loans seem affordable. But just because you qualify for something doesn’t mean it’s a good financial decision. The average car loan is $730 a month, the average mortgage payment is over $2,700 a month, and the average person has close to $7,000 in credit card limits. This is a recipe for financial disaster.

To tackle this, set a budget and stick to it, regardless of what a bank is willing to lend you. When I bought my first home, I was approved for $1.5 million, but I spent $600,000 instead. More recently, I was approved for $6 million, but I bought a $1.4 million home. Spend less, save more, and you won’t be trapped by high monthly payments.

4. Not Understanding Taxes

Most people don’t realize that almost a third of their income goes to taxes. If you don’t take time to understand how taxes work, you’re losing thousands of dollars a year. Some simple ways to lower your tax bill can be making 401(k) contributions, selling losing investments at the end of the year to offset taxes, and, if you have a business, structuring your business as an LLC or S-Corp (if you own one) to save thousands in self-employment taxes. The tax code is designed to reward people who know how to use it. If you don’t want to learn it yourself, hire a professional who can help.

5. Ignoring Retirement Accounts

Just like taxes can cost you money, retirement accounts can save you money. Yet, many people ignore them. The three primary accounts you should be using are:

Roth IRA — which allows contributions up to $7,000 per year with tax-free.

401(k) — which lets you invest up to $22,500 per year pre-tax and reduces your taxable income; and

HSA (Health Savings Account) — which, if you’re eligible, lets you invest $3,850 per year tax-free for medical expenses.

Just by using these accounts, you can shelter over $32,000 per year from taxes without doing anything complicated.

6. Relying on One Source of Income

A report from the IRS found that 65% of millionaires have at least three income streams. Yet, most people only have one source of income — their job. This is risky — if you lose your job, you lose everything. You can consider starting a side hustle, investing in dividend stocks, or buying rental properties to increase your income streams. The more income sources you have, the more financially secure you’ll be.

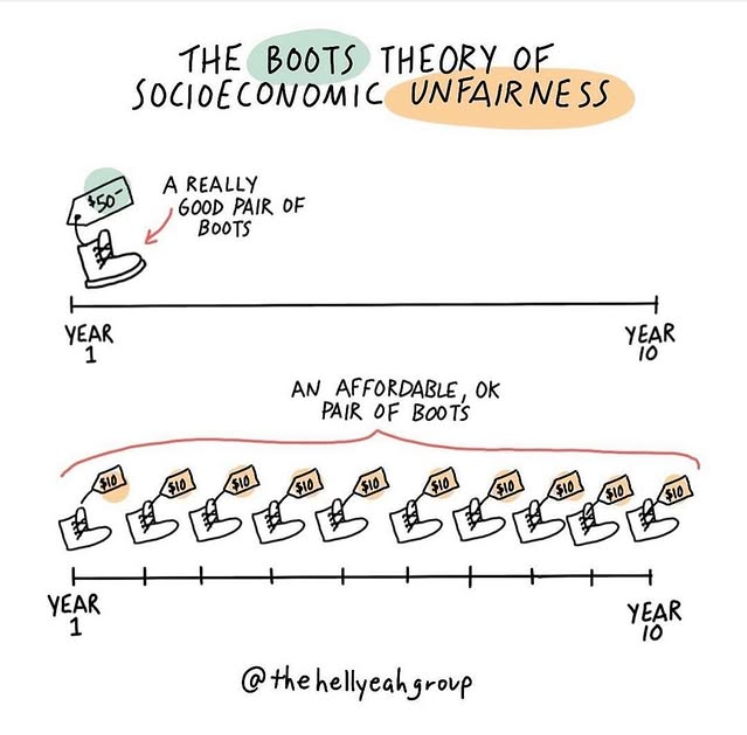

7. Being Too Cheap in the Wrong Places

There’s a big difference between being frugal and being cheap. For years, I made the mistake of buying the cheapest option instead of the best value. For example, I hired a cheap accountant who made costly mistakes. I also bought cheap electronics that broke and had to be replaced. Over time, these decisions cost me more money than if I had just invested in good quality from the beginning.

This is called the Boots Theory — the poor person buys cheap boots that wear out quickly, while the rich person buys quality boots that last a lifetime. Spend money on things that will save you money in the long run.

8. Not Planning for Emergencies

Unexpected expenses will happen. Your car will break down when you least expect it, you might lose your job, and medical bills could come out of nowhere. If you don’t prepare, you’ll be forced into debt. To avoid this, save three to six months of living expenses in an emergency fund, and make sure you have proper home, auto, and health insurance. Being financially prepared for the worst means you won’t have to panic or take on unnecessary debt when things go wrong.

9. Not Having a Financial Plan

Most people have no financial plan. They hope that one day they’ll have enough money, but they have no idea how much they actually need. Think of it like this: when you go on a road trip, you have a map and a destination. But when it comes to money, most people just wing it. That’s a mistake. If you want to be financially free, figure out how much you need to retire, what kind of lifestyle you want, and how much you need to save to get there.

For example, if you want a $1 million home, a nice car, and $5,000 a month in living expenses when you retire, you’ll need about $2 million invested to make it happen. Breaking it down, if you invest $24,000 a year at an 8% return, you’ll reach this goal in 30 years. If you max out your 401(k) and Roth IRA, you’re already on track. You don’t need tens of millions of dollars to be financially free — you just need a number and a plan.

Final Thoughts

Ever since I was a kid, I have been fascinated by what makes someone financially successful. I wanted to understand why some people were good with money while others constantly struggled. As I improved my own finances, it became clear that many people make serious financial mistakes without even realizing it. These nine financial mistakes are incredibly common, but they’re also easy to fix. By avoiding these mistakes, you’ll set yourself up for long-term success — financially and otherwise.

That's it for this week. I hope you enjoyed this article. Let me know your thoughts by responding to this email - I read every single comment :)

Stay safe, stay invested and I will see you next week – Graham Stephan.

A 33 year old real estate agent and investor with over $120M in residential real estate sales. This is my way of sharing actionable ideas that will make you a smarter and wealthier investor.