A 33 year old real estate agent and investor with over $120M in residential real estate sales. This is my way of sharing actionable ideas that will make you a smarter and wealthier investor.

We’ve been waiting for 4 years

Published about 1 year ago • 4 min read

What’s up Graham, it’s guys here :-)

A quick but important note before we get started. Since I shifted to ConvertKit, my newsletter is going to the Gmail promotions tab for some of you. If you find this from the promotions tab, please star the message and drag/move it to the primary inbox :)

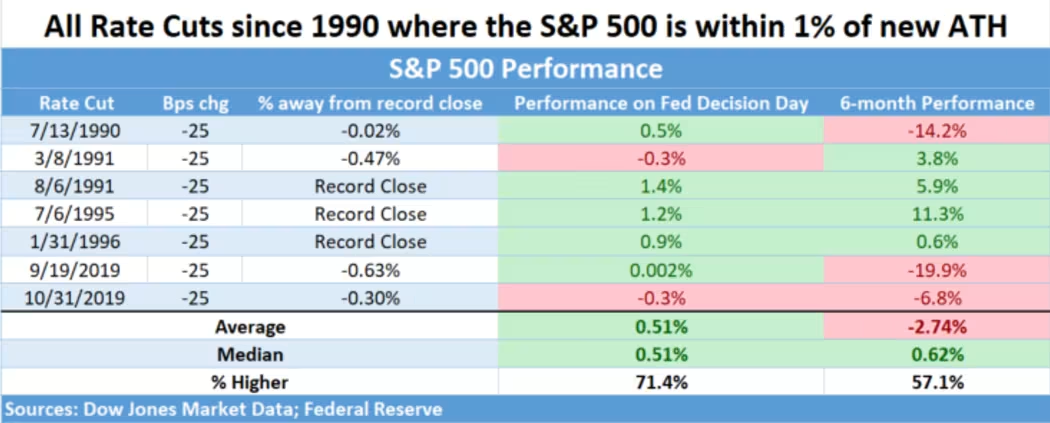

JPMorgan ran the data back 40 years, finding the Fed has cut rates 12 times, with the S&P 500 within 1% of an all-time high. The market was higher a year later, all 12 times, with an average return of around 15%.

Why are we suddenly talking about this again?

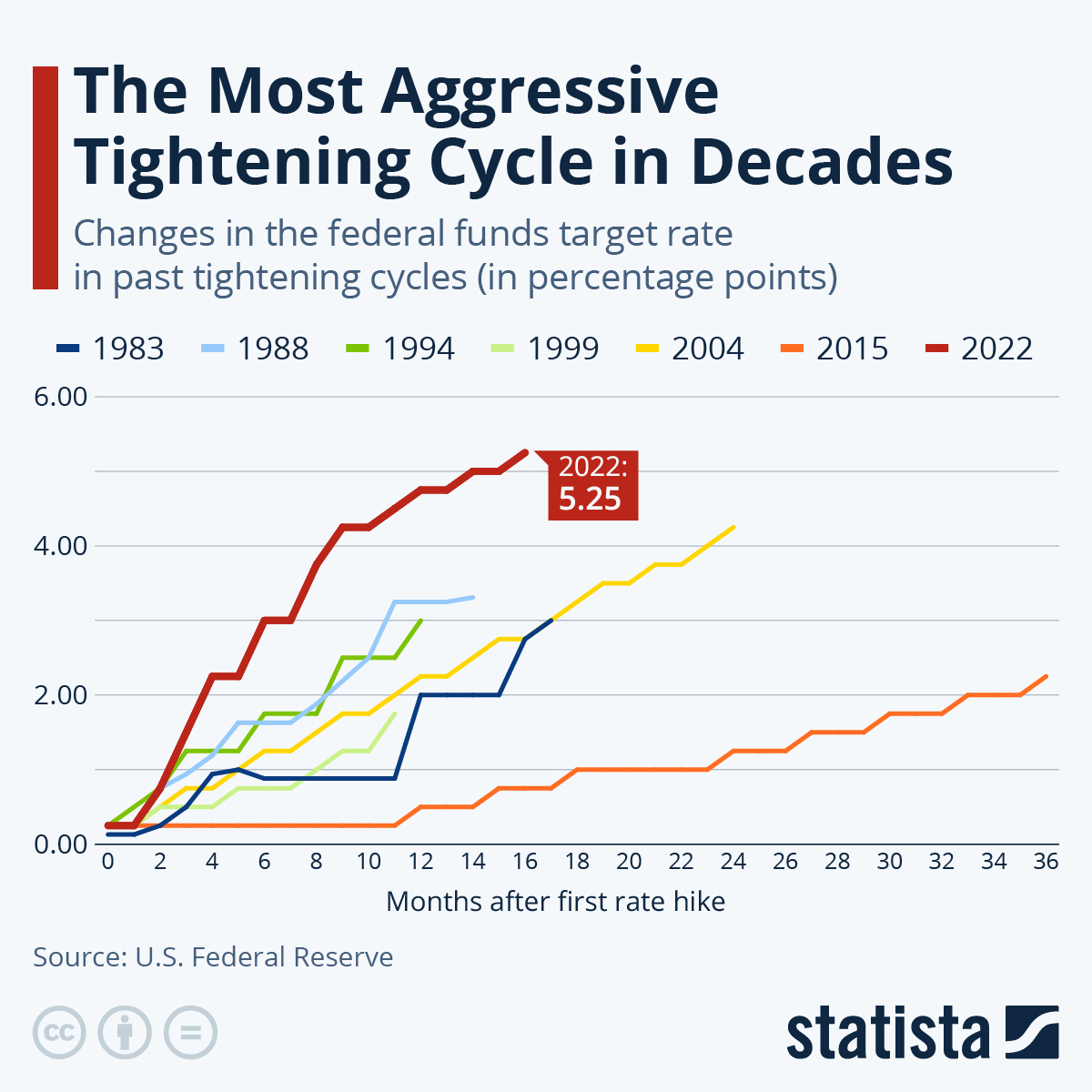

For the first time since March 2020, the Federal Reserve has lowered interest rates by 0.5% after one of the most aggressive tightening cycles in history! This single decision confirms that the Federal Reserve believes inflation is under control and sets a new trajectory that impacts the stock market, housing, national debt, and even your savings account.

So, let’s talk about what the Federal Reserve just announced, the impact this will have on all things money, what history tells us might happen next, and most importantly, how you can use this information to your advantage.

Why the Federal Reserve Lowered Interest Rates

This decision stems from the most recent inflation report by the BLS (Bureau of Labour Statistics). Since February 2020, consumer prices have risen by an average of 21.2%. However, the good news is that prices have recently declined. This allowed the Federal Reserve to cut rates before the economy took a downturn.

In August, inflation rose by only 2%, the lowest level since February 2021, putting the 12-month inflation rate at just 2.5%. Energy prices have fallen by 4%, and oil has dropped by 12.1%. However, core inflation — which excludes food and energy — remains steady at 3.2% due to high housing prices. Housing, which is a lagging indicator, reflects data from the past year, which is why the Federal Reserve may not cut rates as much as some hoped.

Apart from inflation, another important factor led to the Fed’s rate cut -- the unemployment rate.

The Jobs Market's Role in Rate Cuts

The Fed’s main objectives are to support maximum employment and stabilize prices, meaning they aim to control costs without disrupting the economy. The jobs market is a good indicator because it signals how many people are employed, how many jobs are available, and whether wages are strong enough to support the average person.

However, the recent rate hikes have slowed down the job market, with August payrolls showing the smallest gain in three years. There are also fewer available jobs than at any time since January 2021, indicating the rate hikes may have reached their peak.

The Sahm indicator, which has been accurate in predicting recessions, is also well above the 0.5% threshold. For the uninitiated, the Sahm indicator states that if the three-month average unemployment rate rises by 0.5% from its lowest point in the past year, a recession is probably underway.

Source: FRED Real Time Sahm Indicator

What Happens to the Stock Market Now?

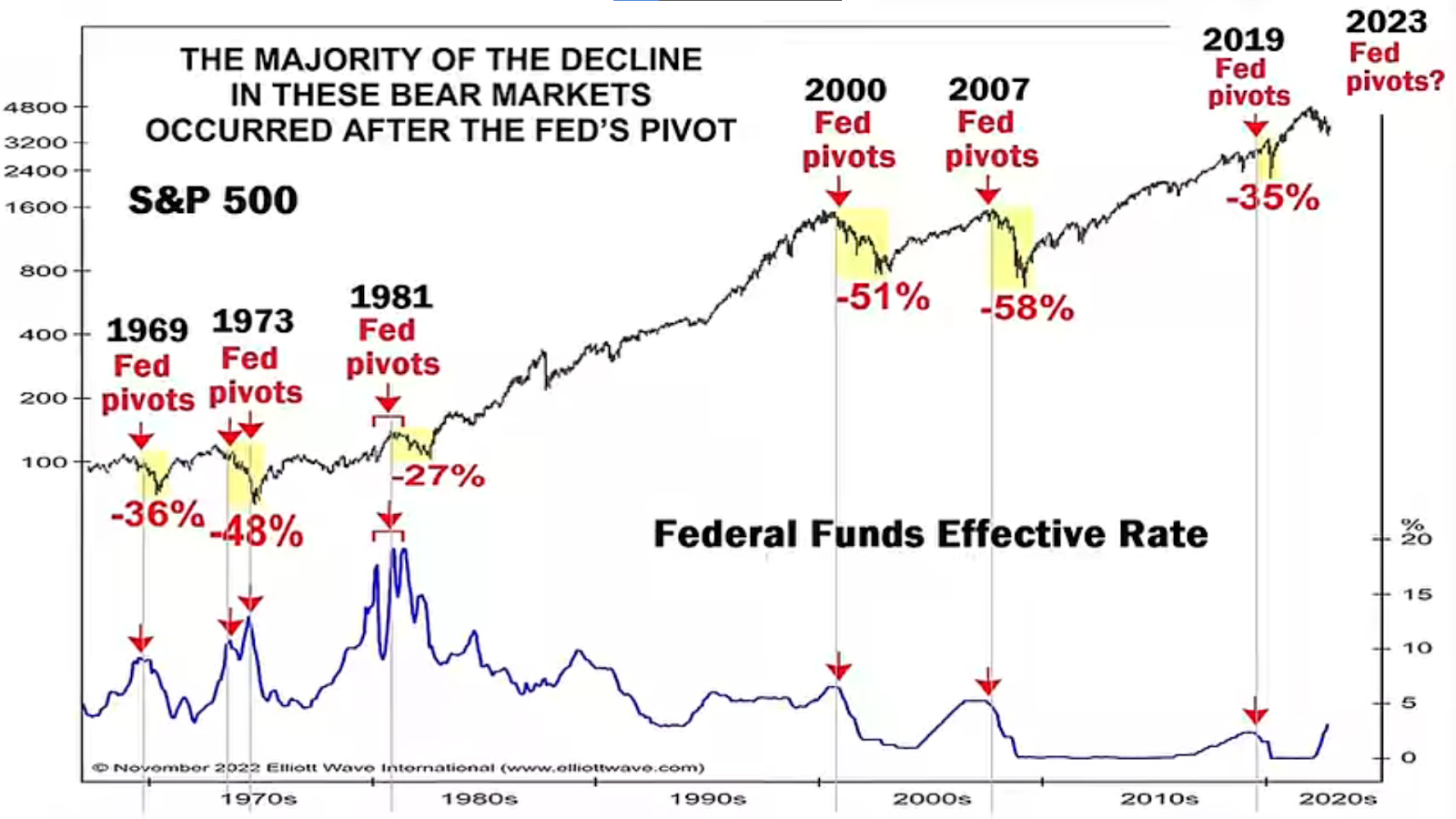

The main question for investors is whether the stock market will go up or down after the rate cut. Lower interest rates typically boost growth, as businesses can borrow more cheaply, thereby increasing profits. But history shows that in the short term, the stock market drops by over 20% every time the Federal Reserve cuts rates.

The reason? The Federal Reserve doesn’t cut rates unless they see warning signs of a downturn. For example, in 2001, they cut rates before the dot-com bubble burst; in 2008, they did so during the Great Recession. So, the rate cuts themselves don’t cause the market to drop — it’s the underlying economic conditions that make the cuts necessary.

Source: Elliott Wave International

However, there’s another school of thought — the Federal Reserve has somewhat trained investors to the point where investors know that they will always step in to save the day if things get terrible. As they say, ‘Any financial or recessionary event jeopardizing the markets would be met withrate cuts and accommodative policy.’ This is why the market has only increased, given enough time, following the rate cuts so far.

Some analysts argue that today’s market already expected rate cuts. Since investors tend to anticipate Federal Reserve actions, the current stock market levels may already reflect the coming changes.

How Will This Impact the Housing Market?

Lower rates generally spark more demand for cheaper mortgages, which could increase housing prices. But despite home prices remaining near all-time highs, there’s good news for buyers: prices are starting to be cut. In July, ~ 19% of listings saw price reductions, causing the median home price to drop from $445,000 to $439,000.

This is largely due to higher mortgage rates reducing demand, with many buyers sitting on the sidelines waiting for rates to drop, which causes sellers to lower their asking prices. However, experts believe minor rate cuts, like the recent one, won’t significantly impact mortgage rates. A 1% drop in rates could qualify an additional 5 million buyers, but the current reduction will only lower mortgage rates from 6.47% to 6.3%, not enough to bring buyers flooding back into the market.

Basically, it's presumed that the Federal Reserve is looking for just the right spot to cut rates enough to keep our economy afloat but not so much that it floods the market with excess demand and sends prices back up again. That's why, for buyers, this rate cut isn't going to have that large of an impact.

In the long run, housing prices will take time to react to rate changes. The Mortgage Bankers Association estimates a 2.9% price increase by 2025, while Fannie Mae projects a 3% rise. For now, buyers have a choice: buy a home at higher rates with less competition or wait for lower rates with more competition.

The Federal Reserve’s Outlook

As of today, the Federal Reserve lowered rates by 50 basis points (0.5%), driven by a weakening job market (caused by the previous rate hikes). Jerome Powell, the Federal Reserve Chair, stated that progress is being made in controlling inflation, and the economy no longer needs such restrictive policies.

According to their projections, rates in 2026 are expected to be significantly lower than they are today, implying that more rate cuts are on the horizon. This is a preventive measure to avoid a possible recession as GDP growth slows and unemployment rises.

Overall, the Federal Reserve is signaling that its approach will be slow and data-dependent. They’re aiming to avoid a recession, which would lead to a stock market decline, a worsening job market, and a sluggish economy. By gradually cutting rates, they hope to stabilize the economy before any significant disruptions occur. Let’s see how this plays out in the coming months.

Until then,

That's it for this week. I hope you enjoyed this article. Let me know your thoughts by responding to this email - I read every single comment :)

Stay safe, stay invested and I will see you next week – Graham Stephan.

A 33 year old real estate agent and investor with over $120M in residential real estate sales. This is my way of sharing actionable ideas that will make you a smarter and wealthier investor.