A 33 year old real estate agent and investor with over $120M in residential real estate sales. This is my way of sharing actionable ideas that will make you a smarter and wealthier investor.

The Problem with FIRE

Published about 1 year ago • 5 min read

What’s up Graham, it’s guys here :-)

Now that my schedule is slightly more flexible, if you’re interested in booking a consulting call and speaking with me directly, fill out the form below to see if it’s a good fit.

I’ll make some time each week to speak with a few of you, one-on-one, about your YouTube channel, Real Estate Deal, Business, or Marketing Strategy (no investment advice). If you’re interested, reach out and I’ll pick a few people to consult with. It can be over a phone call or Zoom (your choice). Thanks for reading!

This is the population pyramid of the United States from the 1960s to 2060 (projected). It shows two metrics — the age and sex of the US population over the years.

Source: Population Reference Bureau Analysis using the US Census Data

Notice that in the 1960s, the population pyramid looked like, well, a pyramid. This indicated a high birth rate and a larger number of younger and working-class adults than older people. But in recent decades, the U.S. has been transitioning toward a more constrictive population pyramid — i.e., lower birth rates and an increasing number of elderly individuals.

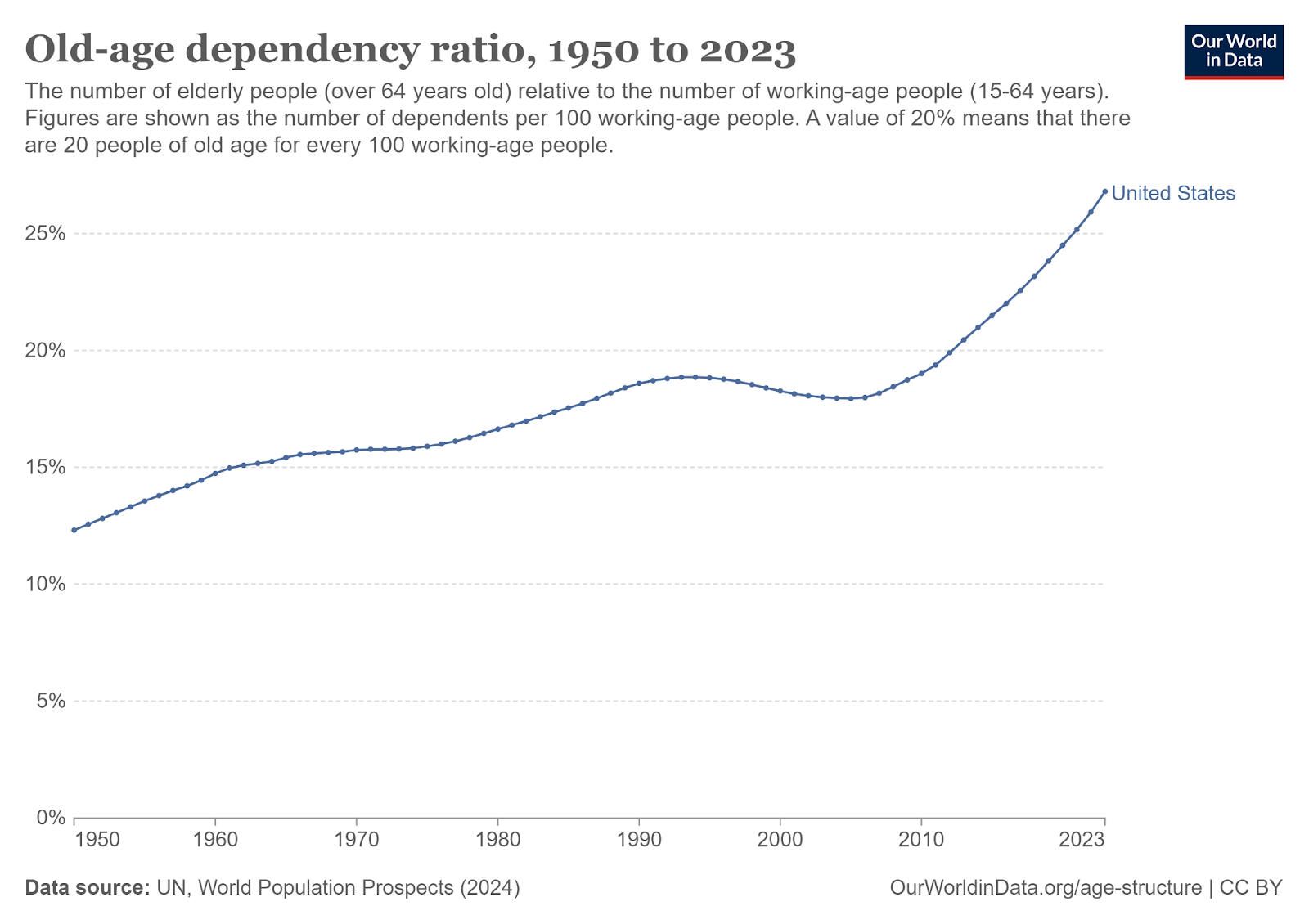

For every 100 people in the working population, there are 'x' number of people outside the working age who depend on them. The lower the 'x', the better. This is called the population dependency ratio.

This ratio has been increasing for quite some time, and this trend points out the growing economic strain on fewer working-age individuals to support younger and older dependents.

This is often overlooked while planning early retirement, but it has significant implications for retirement planning, especially the FIRE movement — Financial Independence Retire Early.

Considering this, we must look at whether early retirement is a sustainable option in light of an aging population. Does the FIRE movement adequately address these potential risks associated with planning for decades of retirement in a world where living longer comes with its own set of financial challenges?

Understanding Financial Independence: What is FIRE?

Financial Independence Retire Early, or FIRE, is a strategy designed to help people achieve financial freedom at a much earlier age than traditional retirement plans allow. The premise is simple -- save and invest aggressively, live below your means, and build enough wealth so that your investments can cover your living expenses for the rest of your life. Once you reach that point, you no longer need to work unless you choose to.

FIRE followers often aim for the ‘crossover point’, a term coined in the book Your Money or Your Life by Vicki Robin and Joe Dominguez. The crossover point is when your investments generate enough income to cover your living expenses fully. At this point, you can step away from full-time work if you wish and live entirely off your investment returns.

Sounds ideal, right? But there’s more to this than meets the eye. While the FIRE movement offers the possibility of financial freedom at a young age, it requires long-term commitment, careful financial management, and an understanding that retiring early doesn't mean an end to life's challenges — just the freedom to face them on your own terms.

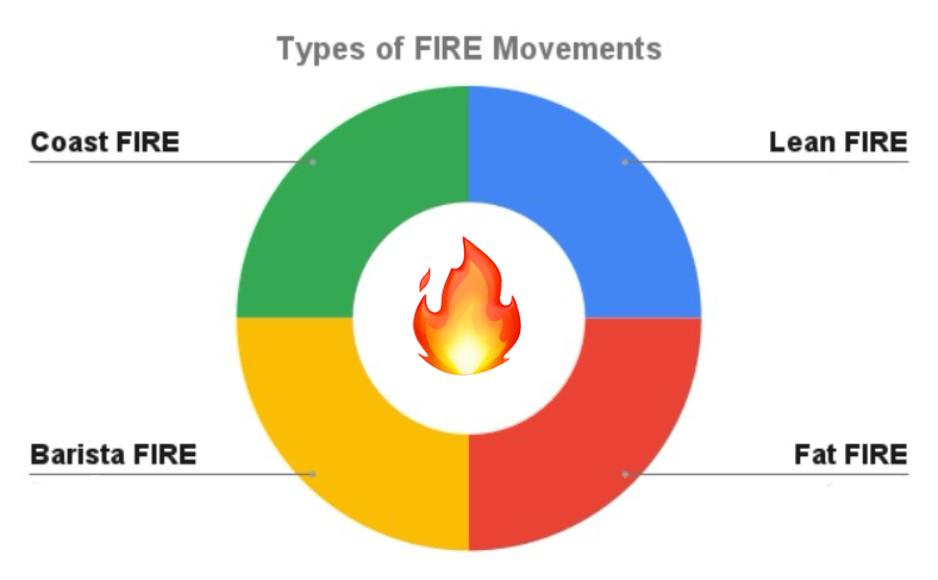

This is why FIRE is not a one-size-fits-all approach. There are several variations that cater to different lifestyles and income levels.

The Different Approaches to FIRE

Lean FIRE: This approach is for individuals who aim to retire on a smaller budget, typically between $30,000 and $50,000 annually. People pursuing Lean FIRE tend to live more frugally and often embrace minimalist lifestyles to reduce their expenses.

Fat FIRE: This is for those who want to maintain a more luxurious lifestyle in retirement. It generally requires savings enough to generate $100,000 or more per year in passive income.

Barista FIRE: Some people aim for a middle ground where their investments cover most of their expenses, but they still work part-time to fill any gaps. This option is more flexible for those who want to balance work and financial freedom.

Coast FIRE: This strategy involves saving aggressively early on, allowing your investments to grow over time without additional contributions. After hitting a certain threshold, you can “coast” to retirement with a less demanding job, relying on your investments to do the heavy lifting.

While these paths offer a road to financial independence, it’s also just as important to acknowledge the challenges that come with it.

The Downsides of FIRE

When talking about becoming financially independent and retiring early, people often talk about the benefits alone and not the drawbacks — exhaustion, overworking, and the pressure (desire?) to save every penny can significantly affect your mental and physical health. But all of these can be classified into two buckets — things that money can buy and things that it can’t. Let’s take a look at them now.

Is Financial Independence the Key to Happiness?

Many expect that they'll finally be happy once they reach financial independence. However, this is a misconception AND one of the main criticisms of FIRE. Financial independence alone doesn’t necessarily lead to happiness. While FIRE may give you the freedom to step away from a 9-to-5 job, it doesn’t automatically solve all of your issues.

If you're unhappy before achieving FIRE, that dissatisfaction may persist even after you've built wealth. Simply having more money won't fix underlying problems related to personal fulfillment, relationships, or mental well-being.

Happiness often comes from having a sense of purpose, engaging in fulfilling activities, and being part of a supportive social network — things that money alone can’t buy.

The Challenges of Extreme Frugality

Another criticism of the FIRE movement is that it can sometimes encourage extreme frugality, which may not be sustainable or enjoyable in the long term. While living below your means is good, some may find themselves sacrificing too much for the sake of early retirement, only to realize they’re not any happier when they achieve it.

For instance, some FIRE advocates focus so heavily on cutting expenses that they miss out on experiences and opportunities that could enhance their quality of life in the present. Striking a balance between saving for the future and enjoying life today is essential for long-term happiness.

How Much Do You Need to Retire Early?

Calculating how much money you need to retire early depends largely on your lifestyle and annual expenses. The most common estimate used by FIRE advocates is the 4% rule. This rule suggests that after retirement, you can safely withdraw 4% of your investment portfolio each year without running out of money. How do you arrive at this number? This is essentially taking your annual expenses and multiplying it by 25. For instance, if you plan to live on $50,000 annually, you would need $1.25 million invested to retire early. For those seeking a more extravagant lifestyle with annual expenses of $200,000, you’d need about $5 million in investments.

The Importance of Mindset: Why FIRE is More Than Just a Number

While many FIRE advocates focus on reaching a specific number, it’s important to remember that financial independence isn’t just about hitting a monetary target. It’s also about finding fulfillment and purpose along the way.

Building wealth and retiring early may give you more flexibility and control over your time, but it doesn’t guarantee happiness. For many, the journey to FIRE is more meaningful than the destination. It teaches valuable lessons about discipline, long-term planning, and prioritizing what truly matters in life.

However, it’s also crucial to avoid becoming too focused on frugality or financial goals at the expense of your present happiness. It’s about balance — enjoying the journey while planning for the future.

Is FIRE Right for You?

At the end of the day, FIRE is not just about retiring early. It’s about having the option to do so. You might reach financial independence and choose to keep working because you enjoy what you do. Or, you might decide to travel, pursue hobbies, or start a business.

While the FIRE movement can seem like an appealing strategy for achieving financial independence and retiring early, it's also essential to factor in the possibility of living much longer than anticipated. You may plan for 15-20 years of retirement, but with increasing life expectancies, there’s a chance you might live for 30+ years post-retirement. This means you must save much more and account for maintaining your lifestyle over several decades.

That's it for this week. I hope you enjoyed this article. Let me know your thoughts by responding to this email - I read every single comment :)

Stay safe, stay invested and I will see you next week – Graham Stephan.

A 33 year old real estate agent and investor with over $120M in residential real estate sales. This is my way of sharing actionable ideas that will make you a smarter and wealthier investor.