A 33 year old real estate agent and investor with over $120M in residential real estate sales. This is my way of sharing actionable ideas that will make you a smarter and wealthier investor.

How should you plan for retirement?

Published 10 months ago • 4 min read

What’s up Graham, it’s guys here :-)

Now that my schedule is slightly more flexible, if you’re interested in booking a consulting call and speaking with me directly, fill out the form below to see if it’s a good fit.

I’ll make some time each week to speak with a few of you, one-on-one, about your YouTube channel, Real Estate Deal, Business, or Marketing Strategy (no investment advice). If you’re interested, reach out and I’ll pick a few people to consult with. It can be over a phone call or Zoom (your choice). Thanks for reading!

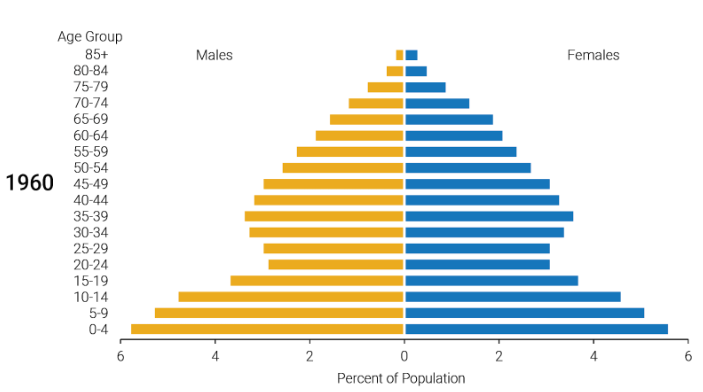

In 1935, the U.S. government enacted a policy to protect Americans from the crushing poverty during the Great Depression. This program aimed to provide financial stability for retired workers, and worked on a simple concept — individuals contributed a small percentage of their salary to the program while working. Upon retirement, they got a steady flow of income. This approach worked great at the time, thanks to a robust workforce. There were significantly more young workers contributing to the system than retirees drawing benefits, creating a sustainable balance.

Source: Population Reference Bureau Analysis using the US Census Data

However, what was once a steady, reliable cushion, now looks more like a ticking time bomb for the shrinking workforce and a growing retiree population. How did we get here, and — more importantly — what happens next?

Social Security’s Looming Crisis: What It Means for You

The reality is that Social Security is hitting closer to home than ever before. With personal savings rates at a 20-year low and Social Security reserves projected to be depleted in less than a decade, many Americans face uncertainty about their financial future. But what exactly is Social Security?

Every time you earn a paycheck, 12.4% of your earnings go toward Social Security, split evenly between you and your employer. This system is designed to ensure that you’ll receive a stable income when you retire. However, Social Security should not be considered a personal savings account. The money you contribute is not saved for your future use; instead, it’s used to pay the current retirees. Future workers will then fund your benefits when you retire. This whole system was designed on the premise that there would be enough young, working people to fund older retirees. Over time, as life expectancy started to increase, this system’s financial stability also came under strain.

The Funding Problem

Today, population growth has slowed down, incomes are barely outpacing inflation, and the ratio of workers to retirees is shrinking. For the first time in U.S. history, older adults are expected to outnumber children by 2034. Fewer workers supporting more retirees creates a funding gap, exacerbating the financial strain. By 2033, it’s projected that Social Security reserves will be exhausted, resulting in a significant reduction in benefits unless changes are made.

If no action is taken, several scenarios are likely:

Benefit Reductions: Monthly checks for retirees could be reduced by 21%.

Increased Retirement Age: The retirement age could be raised, delaying the point at which benefits begin.

Higher Taxes: Social Security taxes may increase to keep the program solvent.

Historically, adjustments like these aren’t without precedent. In 1983, Social Security faced a funding crisis that was resolved by raising the retirement age from 65 to 67.

More recently, France increased its retirement age from 62 to 64 despite widespread public protests. Like the United States, France is also grappling with longer life expectancies, slower population growth, and increasing pressure on its dwindling workforce to sustain retirees. The U.S. may soon face a similar choice, and such measures could be implemented again.

The Value of Your Contributions

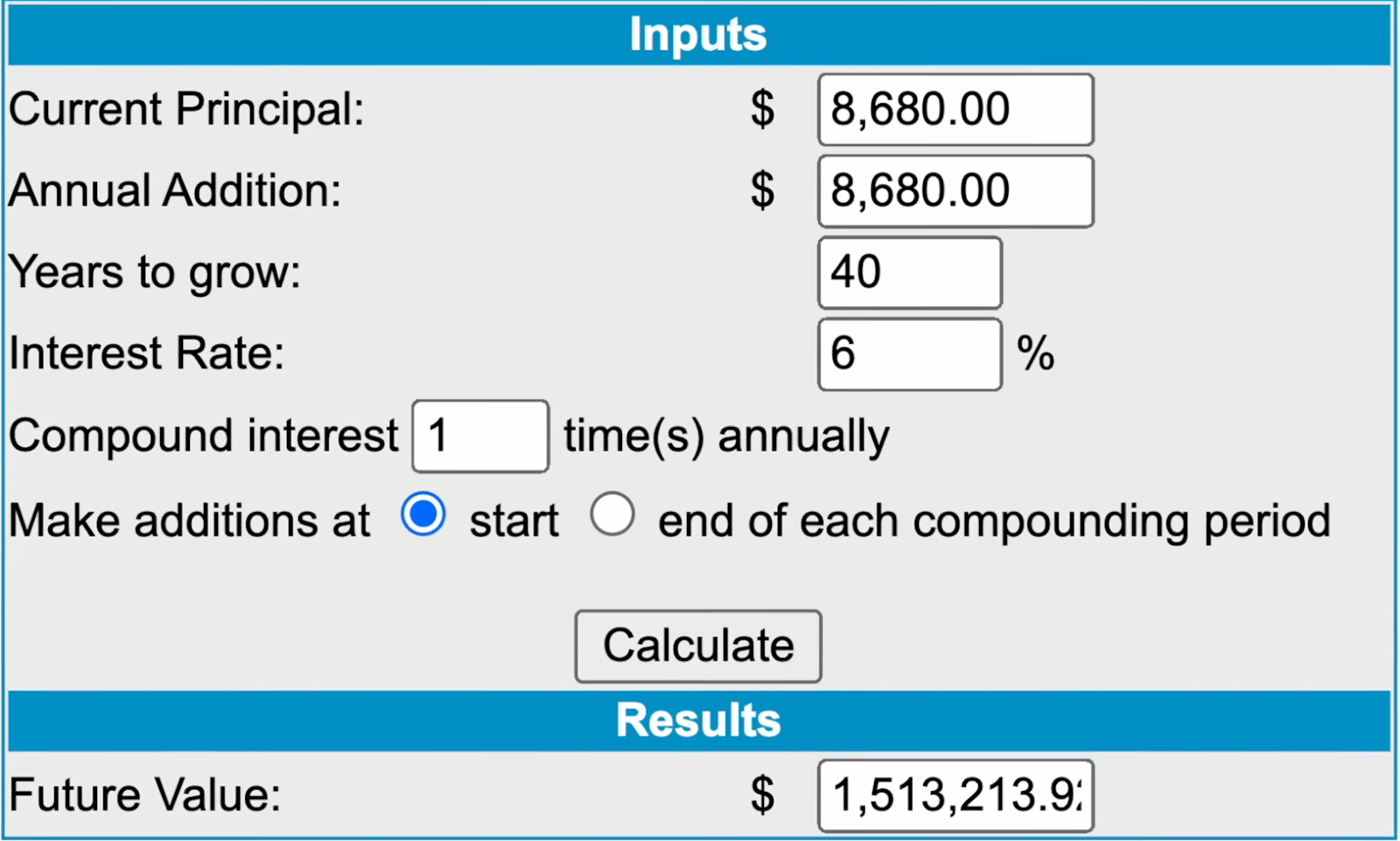

To understand how Social Security compares to investing, let’s crunch the numbers. Suppose you earn $70,000 annually and contribute 12.4% of your income to Social Security for 40 years. If you had instead invested that amount at a modest 6% annual return, you’d have over $1.5 million by age 65, which can easily generate $5,000 per month in income post-retirement.

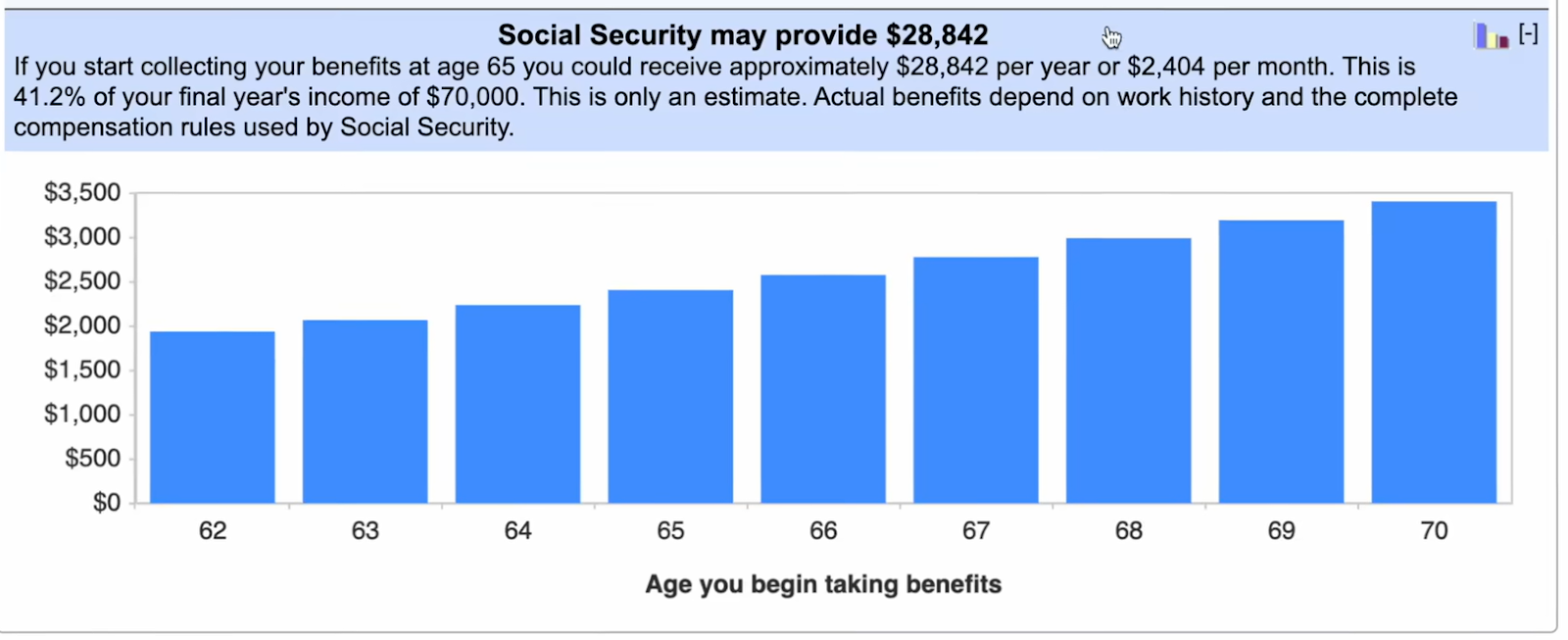

Social Security, by contrast, would provide roughly $2,400 per month — less than half of what you could earn through private investing. While this paints a sobering picture, it’s important to note that Social Security wasn’t designed as a high-return investment. It operates more like insurance, providing a safety net for those who don’t have the means to save or invest adequately.

Source: ssa.gov

Social Security’s investments are limited to safe, low-yield assets such as government treasuries. While this guarantees stability, it also means returns barely outpace inflation — which isn't much, but at least it's guaranteed.

What’s the Solution?

As mentioned before, Social Security operates on a pay-as-you-go model, meaning current contributions fund current retirees. This structure works well when the workforce grows, but as birth rates decline and life expectancy rises, the system struggles to maintain balance.

To preserve Social Security, policymakers are likely to implement some combination of higher taxes and a delayed retirement age. While these changes may feel unfair to younger generations, they’re necessary to keep the system afloat.

One potential change could involve increasing the income cap on Social Security taxes, which is currently $168,000. Any earnings above that amount are exempt from Social Security contributions — a loophole that could be closed to increase funding.

How to Secure Your Financial Future

The best way to protect yourself from Social Security’s uncertainties is to take control of your finances. Here’s how:

Invest Consistently: Start early and invest in a diversified portfolio. Even small contributions can grow significantly over time.

Live Below Your Means: Prioritize saving over spending to build a strong financial foundation.

Plan for Retirement: Aim to save enough to replace your desired annual income. For instance, to generate $50,000 per year in retirement, you’ll need about $1.5 million saved. If you start investing $416 per month at age 20, you can accumulate $1.5 million by age 60, assuming a 7% annual return. The longer you wait, the more you’ll need to save.

Maximize Tax-Advantaged Accounts: Utilize tools like Roth IRAs and 401(k)s to grow your investments tax-free.

Final Thoughts

While Social Security provides a vital safety net, it’s not a replacement for personal financial planning. Relying solely on the government for your retirement is risky, especially given the program’s uncertain future.

Take proactive steps to secure your financial independence. By investing early, living frugally, and maximizing your income, you can ensure a comfortable retirement — regardless of what happens with Social Security. Recognizing its limitations will encourage you to prepare for a future where Social Security is a supplement, not the sole source of your retirement income.

That's it for this week. I hope you enjoyed this article. Let me know your thoughts by responding to this email - I read every single comment :)

Stay safe, stay invested and I will see you next week – Graham Stephan.

A 33 year old real estate agent and investor with over $120M in residential real estate sales. This is my way of sharing actionable ideas that will make you a smarter and wealthier investor.