What’s up Graham, it’s guys here :-)

I’m now taking consulting calls and offering one-on-one sessions to help with your YouTube channel, Real Estate Deals, Business, or Marketing Strategy (no investment advice).

If you’re interested in booking a call, fill out the form below to see if it’s a good fit. I’ll personally review submissions and select a few people each week for a consultation. These sessions can be held over the phone or via Zoom — your choice.

In 2008, just as the housing market was about to hit a freefall, I watched a friend sign the papers on what seemed to be her dream home. She’d saved diligently for the down payment and believed she was prepared for everything — until the first round of property taxes and unexpected repairs arrived. Just then, as the bubble burst, she found herself locked into the same mortgage payments even though the house’s value had sunk far below her purchase price. Suddenly, the mortgage payment was only a fraction of what she actually needed to cover each month. Affording a house involves far more than just qualifying for the loan.

And it’s not just about owning, either — even renters face their own set of financial surprises, especially in high-cost areas where rent can eat up over half your paycheck. In today’s market, interest rates are higher, property prices remain steep, and lender guidelines are not really reflecting the new economic reality. So the real question is: how do you figure out the true cost of a home, whether you’re renting or buying?

As someone who has worked in real estate full-time since 2008, I’ll break down the numbers behind renting and owning, highlight the common pitfalls that can drain your wallet, and share my personal insights on how you can be better off. By the end, you’ll have a clearer picture of which path fits your lifestyle — and your bank account.

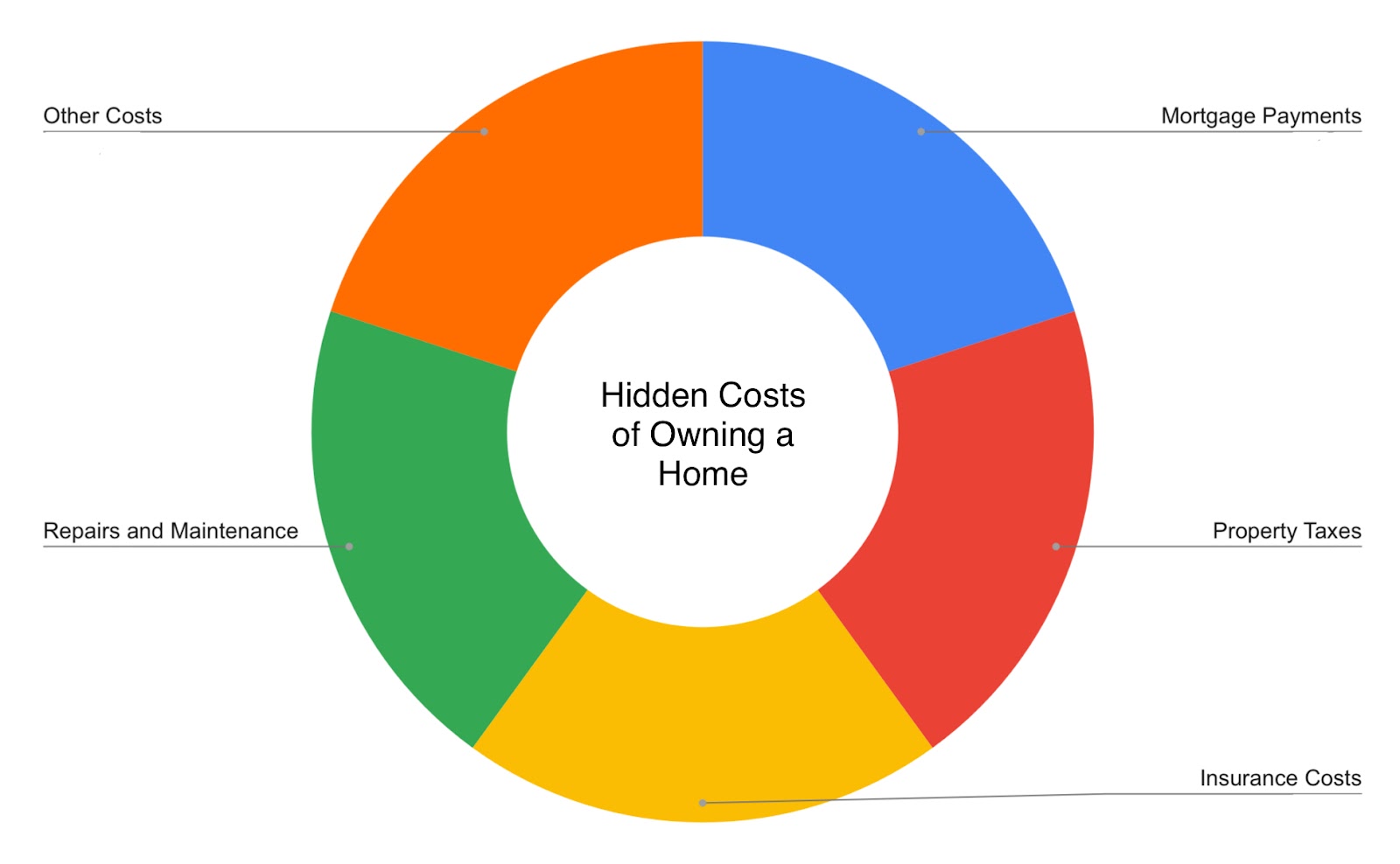

Hidden Costs When Buying a House — Is it worth it?

When it comes to housing expenses, renting and buying are fundamentally different. Renting is often straightforward: you pay a fixed amount every month, with no surprise costs for repairs, property taxes, or insurance. In contrast, homeownership comes with additional expenses that can quickly add up, making it much more complex.

For instance, owning a home involves:

- Mortgage Payments: This is usually a mix of principal and interest amortized over 15–30 years. Fixed-rate loans keep payments steady, but they’re just the beginning.

- Property Taxes: Based on a percentage of your home’s assessed value, property taxes can range from 0.4% to 2% annually and often increase over time.

- Insurance Costs: Lenders require comprehensive insurance to cover potential damages.

- Repairs and Maintenance: From fixing a water heater to replacing a roof, homeowners often spend 1% of the home’s value each year on upkeep.

- Other Costs: HOA fees, landscaping, cleaning, and unexpected expenses.

All of this makes owning a home substantially more expensive than renting. These additional costs are equally important when evaluating what you can afford.

The Cost of Renting: A Simpler Equation

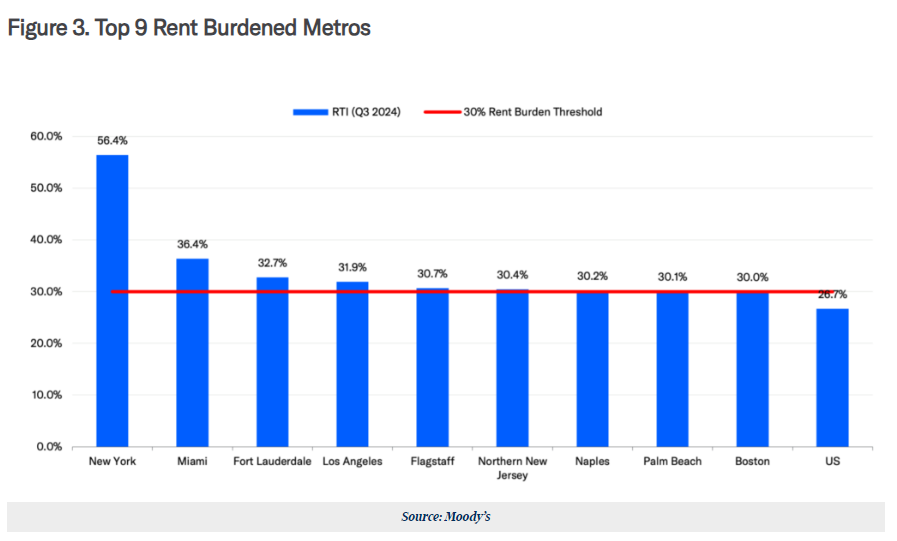

For renters, the traditional rule of thumb is that housing expenses should not exceed 30% of your gross income. However, this was developed decades ago and doesn’t account for today’s realities, such as student loan debt or high transportation costs. I prefer an alternative — the 50/30/20 budget rule suggests spending no more than 50% of take-home pay on needs (including housing), 30% on wants, and 20% on savings or debt repayment.

In high-cost areas like New York, renters often spend over 55% of their income on housing. In these extreme cases, a more practical approach could be backward budgeting — accounting for fixed expenses, savings, and discretionary spending first, and then allocating what remains to rent. Ideally, aim to keep rent below 20% of your gross income for a healthier financial balance.

Buying a Home: The Financial Guidelines

Buying a home is a major financial decision that requires fore-thought & planning. And one of the most common principles is the 28% rule. This states that you should spend no more than 28% of your gross monthly income on your mortgage payment, property taxes, and insurance. For example, if you earn $60,000 annually, this guideline supports a monthly payment of $1,400. At a 6.5% interest rate with a 20% down payment, this translates to a home valued at approximately $215,000.

A more conservative approach is the 30/30/3 rule. First, you should spend no more than 30% of your gross income on your mortgage. Second, you should save 30% of the home’s value in cash, allocating 20% for the down payment and 10% for emergencies. Finally, you should avoid purchasing a home that costs more than three times your annual income. This framework ensures that you maintain a financial buffer while purchasing a home within your means.

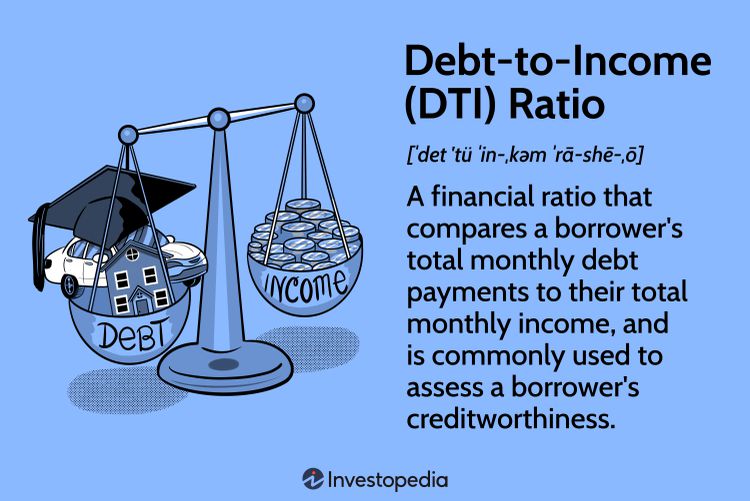

Lenders also use the debt-to-income (DTI) ratio as a key metric to evaluate mortgage eligibility. Generally, a DTI ratio below 45% is ideal, meaning your total debt payments — including the mortgage — should not exceed 45% of your income.

These are some guidelines that will ensure that you don’t overextend yourself financially. Still, lenders may approve loans that exceed these limits, which can lead to risky situations if your income doesn’t increase as expected.

Renting vs. Buying: Which Makes More Sense?

In many parts of the country, renting is currently more affordable than buying. A recent study found that the average cost of owning a home is 25% higher than renting. While owning can be a great long-term investment, renting might be the smarter short-term option if you can’t find a property that fits your budget or long-term plans.

On the other hand, buying can make sense if you plan to stay in a home for at least 10 years or find a good deal. In those cases, the financial benefits of homeownership often outweigh the costs.

That said, if you are planning to purchase a house in 2025, here are some important tips to follow:

Tips for Aspiring Homeowners

- Shop Around for the Best Mortgage Rate: A lower interest rate can save you thousands of dollars over the life of your loan.

- Negotiate with Sellers: Especially in a buyer’s market, don’t be afraid to ask for price reductions, repairs, or closing cost assistance.

- Be Prepared for Repairs and Maintenance: Expect the unexpected and keep an emergency fund for home-related expenses.

- Buy for the Long Term: Avoid short-term purchases unless you’re confident you can sell or rent the property profitably.

Understanding the costs of renting and buying is essential for making informed financial decisions. Renting offers simplicity and flexibility, while buying provides stability and potential long-term returns. The best choice depends on your goals, location, and financial situation.

By following these guidelines, saving diligently, and planning for the unexpected, you’ll be well on your way to affording the home of your dreams — whether it’s a modest starter house or a luxurious estate.

I’ve had the privilege of working with incredible people through my consulting calls, and the feedback has been amazing. Many have shared how these sessions provided clarity, actionable strategies, and a fresh perspective on their projects — from growing their YouTube channels to figuring out business & real-estate deals.

It’s been incredibly rewarding to see these successes, and I’m excited to continue helping more people achieve their goals. If you’re interested, fill out the Google Form to get started. I look forward to connecting with you!

That's it for this week. I hope you enjoyed this article. Let me know your thoughts by responding to this email - I read every single comment :)

Stay safe, stay invested and I will see you next week – Graham Stephan.

113 Cherry St #92768, Seattle, WA 98104-2205

Unsubscribe · Preferences