Hey there! Just a quick announcement:

Since I’ve started posting slightly less, I’ve been inundated with people asking if I’d offer YouTube, Business / Marketing, and Real Estate consulting. I recently did one-on-one calls with a few readers and it went incredibly well. I enjoyed talking to them a lot too. Now that my schedule is slightly more flexible, if you’re interested in booking a consulting call and speaking with me directly, fill out the form below to see if it’s a good fit.

I’ll make some time each week to speak with a few of you, one-on-one, about your YouTube channel, Real Estate Deal, Business, or Marketing Strategy. I’m not sure how long I’ll do this for, or if it’s feasible to continue long-term - but, if you’re interested, reach out and I’ll pick a few people to consult with. It can be over a phone call or Zoom (your choice). Thanks for reading!

Disclaimer: Obviously, I won’t offer financial or investment advice. This is directed towards people with specific questions about their business, marketing, real estate, or YouTube channel. Any financial advice questions will be ignored and I will not get back to you.

A new study found that 90% of millennial homeowners have regrets about their first home purchase.

If you thought it couldn’t get worse, yes, it can -- Millennials are doing better than average because overall, 93% of buyers had regrets about their home purchase in 2023.

Unlike previous years, I have a feeling these regrets will only continue, especially with the housing market facing an affordability crisis, an inventory shortage, and record-high mortgage rates. This makes me wonder: Is buying a home even worth it in 2024?

That’s why we need to discuss what’s happening, why so many homeowners are now regretting their purchase, what you can do about this to avoid losing money, and finally, the five most common mistakes that almost everyone makes when they buy a home.

Housing Market – The story so far

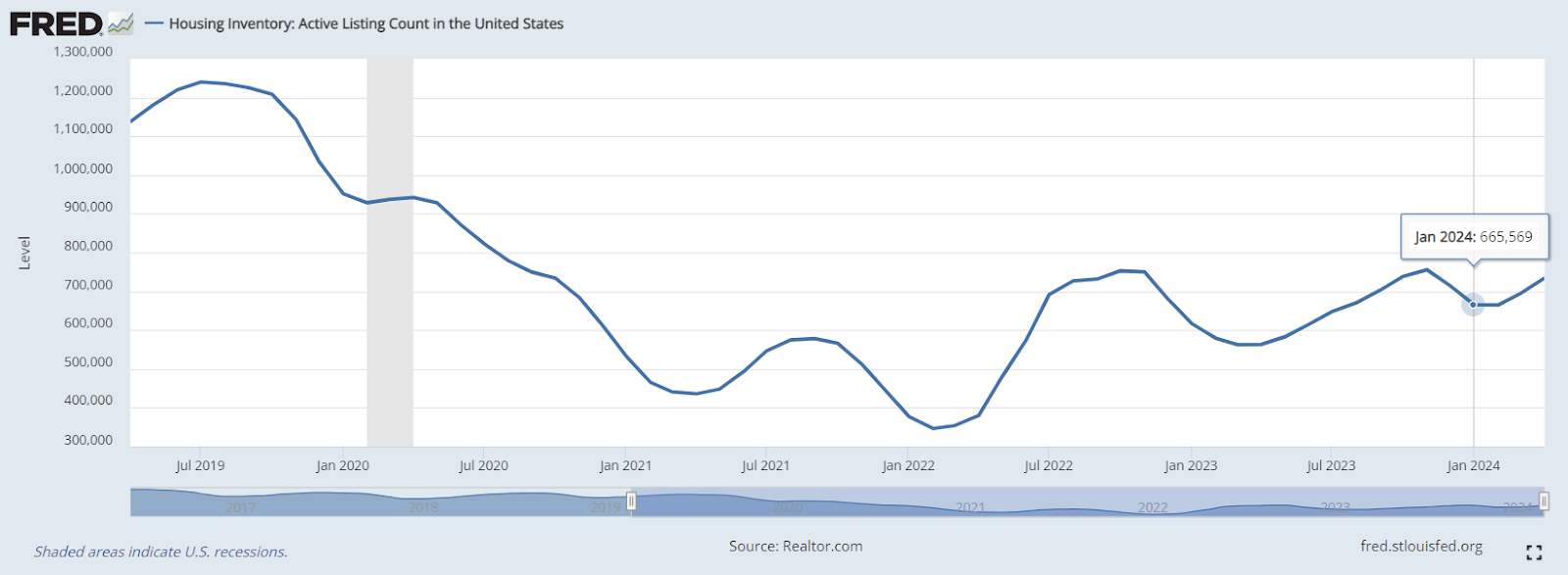

As a bit of background, here’s what you need to know about the housing market because this will explain a lot. Year over year, national home prices are up 5%, mortgage rates have increased from 6.6% to 6.75%, and active listings have barely risen from 616,000 to 665,000 units.

This is still just a third of the number of homes available back in 2016. This creates a challenging market for both buyers and sellers --

- No seller wants to move and give up their existing mortgage rate, leading to low inventory, and

- The average buyer now needs to make $115,000 per year to afford the typical home.

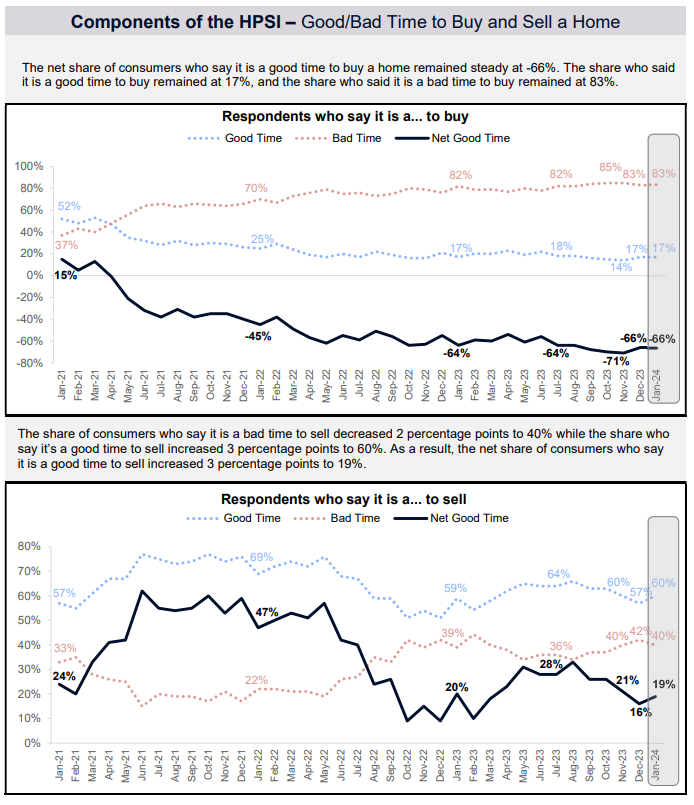

It’s almost like a “chicken or the egg” scenario where prices won’t come down without interest rates being low enough to incentivize homeowners to sell, but lower interest rates would drive more demand, pushing prices even higher. A whopping 83% of people surveyed said that now is a bad time to buy a home, and 60% say it’s a good time to sell a home.

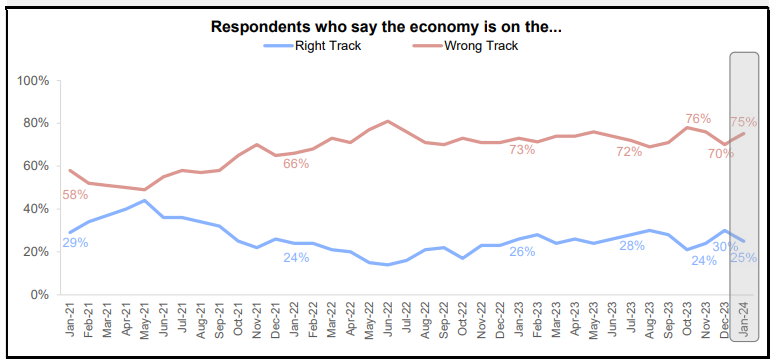

Even worse, 75% believe that the economy is on the wrong track, the highest amount reported since 2021. Home buying sentiment has not been this low since 2012 when the market was just starting to recover from the Great Financial Crisis. This is only worsened by the fact that 81% of workers don’t believe their current wage has kept up with the rising cost of living.

This survey shows that 39% expect to pay a higher interest rate than they’d like, 36% are prepared to make multiple offers, 30% plan to max out their budget, and 29% are ready to pay more than a home’s asking price.

What can you do to make sure you don’t fall into the same trap?

Common Homebuyer regrets

Regret #1 – Too much maintenance

The first homebuyer regret, according to 33% of respondents, was that their home requires too much maintenance. It’s important to mention that home maintenance was never quite the regret it is today.

Last year, only 25% of homeowners regretted the overwhelming cost of maintenance. Repair costs are higher. Zillow revealed that homeowners can expect to pay $14,155 a year, or $1,180 a month, in hidden costs related to owning a home.

Average home maintenance costs increased by $400 year on year, now coming in at $6,548 per year. Supply shortages, labor costs, and inflation are driving up the price of everything

There’s a saying that goes like, “Rent is the most you’ll pay every month, but a mortgage is the least you’ll pay” and this is extremely true. Everything in a property has a lifespan until it needs to be repaired or replaced. Roofs generally last 15-25 years, water heaters last 10-15 years, AC units last 10-15 years, and garbage disposals break every few weeks. When you average those costs over the course of homeownership, it starts adding up.

To prevent financial surprises, get a comprehensive inspection report when buying a home. This should uncover many issues before they need to be addressed. Expect that home maintenance will cost you an average of $500-$600 per month or 1% of the home’s value every year. As a homeowner, those once every 10-15 year costs will easily eat away at your savings.

Regret #2 – Buying Too Quickly

The second home-buying regret, felt by 30% of respondents, was buying too quickly. Many buyers simply got impatient and jumped on something that wasn’t the ideal match. Millennials translate this to 27% owning in a bad location and 26% having bad neighbors.

Homeownership is never something to rush into. It’s one of the biggest purchases you’ll make in your lifetime, and that’s not something to jump into because you’re impatient.

In a highly competitive market, there will be some compromises. Millennials, in particular, are more likely to buy a home near an airport, train tracks, or busy highway. But it’s unlikely you’ll live in that house for the next 50 years. On average, you’ll probably be moving somewhere else in 13 years or less.

If you’re buying a home, spend time getting to know the area before you buy. Visit the home, meet the neighbors, and learn about the neighborhood problems before committing.

Regret #3 – Paying Too Much Money

The third regret is spending too much money -- Roughly 38% of homebuyers said they paid over the asking price in 2023. Additionally 22% regret that their mortgage is too expensive.

From my own experience, the first loan estimate you get is not going to be the lowest price. It’s up to you to shop around for a more competitive offer. Banks won’t budge until you present them with another, lower offer. They need “reasonable proof” that they’re not lowering the rate for the sake of saving you money at their expense.

If you’re trying to get the best interest rate, get one quote, take it to a second lender, have them beat it, take that to a third lender, and repeat the process until your rate won’t go any lower. Buyers who do this save an average of $84,000 over the lifetime of the loan.

In a market like this, it’s best to have a strict budget in mind ahead of time and only pay up to the point where you wouldn’t regret walking away. This prevents buyers from getting caught in the moment and overpaying.

Regret #4 – Buying a Fixer-Upper

The fourth home buying issue is 26% of buyers regretting buying a fixer-upper. Fixer-uppers became a popular alternative for first-time homebuyers because they usually came at a cheaper cost with less competition. However, you need to know what you’re doing, or you will get in trouble.

Anytime you buy a fixer-upper, assume two things will always be true:

- Your project will cost at least 25% more than you anticipate, and

- It will take twice as long to finish.

Across every single renovation I have overseen, there are very few times that a project comes in under budget or within the originally quoted timeframe.

Plus, once you start renovating, even if it’s something minor, it becomes exponentially easier to take on more. For example, if you’re remodeling the kitchen cabinets, you may as well replace the countertops. But while they took out the cabinet, they discovered water damage that also needed to be repaired. It’s never-ending.

Buying a fixer-upper is not a bad idea -- It’s one of the best ways to buy a property under market value and make it exactly how you like it without paying a premium. However, go in with the proper expectations, and stick with the plan once you start. If you budget that it’ll be around 35% more expensive and take twice as long, you’ll probably be fine.

Buying a home is a significant investment and should not be rushed. Homeownership can be a good investment, but it requires careful planning and realistic expectations.

All of this seems absolutely pointless when you realize that unless you’re planning to live in the home for at least 10-15 years, renting is cheaper in most areas.But this isn’t new – buyers have had regrets at least since 2019, when this was the case for 81% of homeowners which is lower than today but still pretty high. To avoid common homebuyer regrets, consider the following advice:

- Plan for Long-Term Ownership: Buy a home with the expectation of living there for at least 8-10 years. Otherwise, the costs of buying and selling cancel out the benefits of a mortgage.

- Understand Your Motivation: Be clear about why you’re buying a home. Whether it’s to save money, put down roots, or make an investment, ensure your purchase aligns with your goals.

- Stay Within Your Budget: Never max out what you’re able to afford. This way, you’ll have a financial cushion in case you’re surprised.

As a first-time home buyer, you’ll need to make sacrifices, and that’s just a part of life. You won’t get the home you’ve always wanted, and that’s okay. Use this as a stepping stone to learn, get used to the idea of home ownership, you can slowly trade your way up to the place you’ve wanted over time.

That's it for this week. I hope you enjoyed this article. Let me know your thoughts by responding to this email - I read every single comment :)

Stay safe, stay invested and I will see you next week – Graham Stephan.

113 Cherry St #92768, Seattle, WA 98104-2205

Unsubscribe · Preferences