A 33 year old real estate agent and investor with over $120M in residential real estate sales. This is my way of sharing actionable ideas that will make you a smarter and wealthier investor.

Here's how I'm Building Passive Income

Published about 1 year ago • 5 min read

What’s up Graham, it’s guys here :-)

A quick but important note before we get started. Since I shifted to ConvertKit, my newsletter is going to the Gmail promotions tab for some of you. If you find this from the promotions tab, please star the message and drag/move it to the primary inbox :)

Here's a quote by Benjamin Graham that resonates with me: One of the most persuasive tests of a high-quality (company) is an uninterrupted record of dividend payments going back over many years.

Dividend investing is one of the strategies that doesn’t hinge on the market’s volatility. Instead, it works quietly in the background, compounding over time and helping you grow your wealth steadily. While it may not sound as exciting as the latest stock trending on r/WallStreetBets, it has the potential to build long-term wealth.

So, in this week’s newsletter, let’s discuss whether dividend investing is worth it, how much you’ll realistically need to replace your income, and my dividend portfolio, which currently generates almost $10,000 a month!

Dividend Basics

For those unfamiliar, anytime you buy a stock, you’re entitled to a portion of that company’s profits. Sometimes, these profits are reinvested into the company for its growth. But sometimes, profits are distributed regularly as dividends. This dividend is nothing but a fixed amount that each share pays out, usually every quarter, and the percentage return is based on the stock’s current trading price.

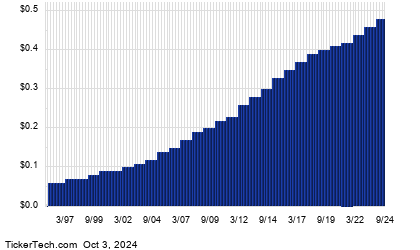

For example, if a share pays $5 a year and is trading at $100, the current dividend yield is 5%. The dividend yield can fluctuate depending on the stock price. Not all companies pay dividends, but those that do are often more mature, where reinvesting capital into growth no longer provides as high a return. Depending on the company, dividend yields can range from 1% to 10%. This type of passive income can be one of the most straightforward and predictable forms of cash flow you’ll ever generate. For instance, here’s the dividend growth chart of Coca-Cola from the year 1997:

Source: Dividend Channel

So, from an investment standpoint, dividends provide regular, predictable cash flow without requiring you to sell shares. This means you have more income to reinvest in other opportunities. However, just like any investment strategy, you must consider its advantages and disadvantages. Here are some points I considered before investing in a dividend-yielding stock or ETF.

The Pros of Dividends:

Predictable Cash Flow: Dividends are more predictable than the stock market itself. Regardless of whether the stock price goes up or down, you still receive the same dividend payment. This provides consistent cash flow, smoothing out market fluctuations. *cough cough* Warren Buffet *cough cough*

Less Volatility: Dividend payments tend to be much less volatile than stock prices. From 1900 to 2018, dividend payments showed an average variance of only plus or minus 10% during market downturns, while stock prices were far more erratic. This makes dividends especially appealing for those seeking stable returns.

Potential to Increase: In some cases, dividend payments can even increase during recessions. For example, in three of the recessions since 1900, dividends grew, with a 46% increase following World War II. Even when dividends are cut, it’s often by much smaller margins compared to the stock market’s decline.

Dividend Contributions to Market Returns: Dividends have historically accounted for a significant portion of market returns, particularly during periods of high inflation. Fidelity reports that dividends contributed 54% of market returns when inflation exceeded 5%.

The Cons of Dividends:

Dividends Are Not Guaranteed: Companies can reduce or eliminate dividends during tough times, as they’re often a reflection of a company’s profits. When the company generates losses or insufficient profit, dividends may be suspended until conditions improve.

Stock Price Decline Risk: A dividend won’t protect you if the stock price declines significantly. For instance, earning a 5% dividend won’t help if the stock itself drops by 30%. This risk is real, as seen with companies like 3M, which currently offers a 5.6% dividend but has lost over 55% of its value over the past five years.

Taxation: Dividends are taxed the moment you receive them, unlike stocks, where taxes are only due when sold. This could mean paying 20% or more, depending on your tax bracket. Dividends also face double taxation -- once at the corporate level and again when distributed to shareholders.

Irrelevant to Value Creation: Some economists argue that dividends don’t create additional value for a company. In theory, when a company pays out a dividend, the company’s stock price should get adjusted by an equivalent amount, keeping your overall value the same.

Now that we have considered the pros and cons, here’s how to optimize your portfolio for dividends.

How to Invest for Dividends

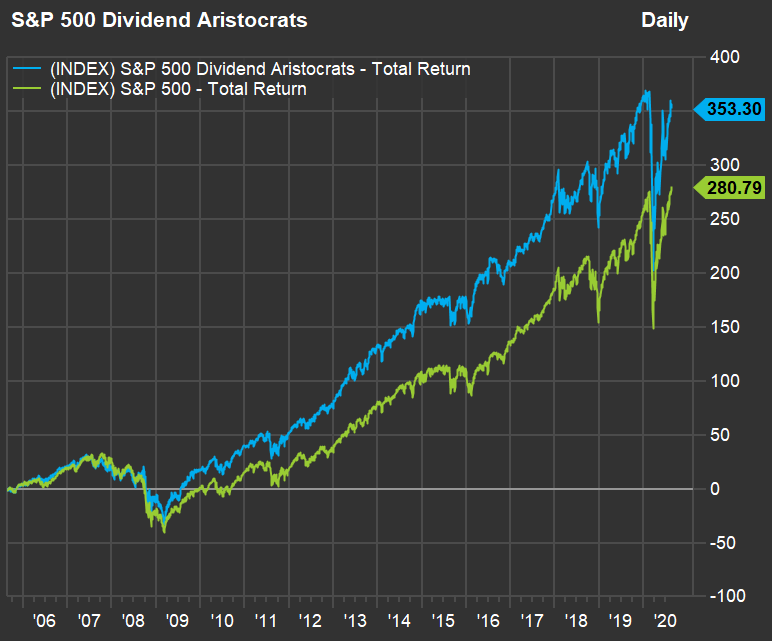

When investing in dividends, it’s essential to think long-term. While you might want to chase high yields, consistency is key. This is exactly where dividend aristocrats come in. These are S&P 500 companies with over 25 years of consecutive dividend increases. Historically, they outperform during recessions and continue to grow their dividends.

The average dividend aristocrat yields between 2% and 3%. If you aim to replace an income of $50,000 a year, you’d need approximately $1,670,000 invested in a basket of these stocks, assuming a 3% yield. Achieving this could be done by investing $5,000 a year over 40 years, while reinvesting dividends. And remember, apart from the dividend yield, the stock/index also grows over time. This can increase your returns by an even higher margin.

Source: Market Watch

For those looking for higher yields, there are alternatives like covered call ETFs such as JEPI, which can yield up to 10.7%. While this option provides substantial income, it comes with the risk of limited upside potential during bull markets and potential downside if the market drops. This method could potentially replace a $ 50,000-a-year income with just $500,000 invested, but it’s not without its risks. Here’s what I do:

My Dividend Portfolio

In terms of my personal portfolio, I currently receive close to $10,000 a month from three main sources:

Broad U.S. Market ETF (SCHB): With a 1.56% yield, this ETF covers 2,500 of the largest publicly traded U.S. companies. I have over $3.8 million invested here, generating about $5,000 a month in dividends.

International Equity ETF (SCHF): This ETF has a 2.65% yield and includes large and mid-cap stocks from developed countries outside the U.S., such as Nestle, Samsung, and Toyota. I have nearly $1 million invested, which brings in an additional $2,000 a month.

Individual Stocks: I also hold a variety of individual stocks that further contribute to my dividend income, adding up to a total of about $9,400 in dividends every month, or roughly $112,000 annually.

*Note: This also depends on your average price and not just the current market price.

Conclusion

Living entirely off dividends is achievable, but it requires careful planning and a diversified portfolio. While dividends offer great benefits like predictable income and tax advantages, they also come with risks, like the potential for dividend cuts or stock price declines.

For anyone looking to replace their income with dividends, it’s essential to think long-term and be mindful of the risks involved. Dividends can be a great addition to a well-rounded investment portfolio, but they shouldn’t be the sole focus unless you’re close to or already in retirement.

That's it for this week. I hope you enjoyed this article. Let me know your thoughts by responding to this email - I read every single comment :)

Stay safe, stay invested and I will see you next week – Graham Stephan.

A 33 year old real estate agent and investor with over $120M in residential real estate sales. This is my way of sharing actionable ideas that will make you a smarter and wealthier investor.